It’s All Happening In Jamshedpur!

When I read this article on Hydrogen Fuel News, which is entitled Cummins And Tata Motors Ignite Change With H2 Internal Combustion Engines, I couldn’t resist using the jokey headline, which was inspired by the sub-heading.

The manufacturing has started in Jamshedpur, India at a new state-of-the-art facility

These two paragraphs give some more details.

The hydrogen internal combustion engines continuing to be produced at the facility are being integrated into Tata Motors trucks. This technology is being viewed as a promising zero- or low-carbon alternative to diesel power because of its powerful performance and substantial operating range.

Cummins’ B6.7H engines have notable similarities to current natural gas and diesel engines, particularly in terms of the components they contain. Moreover, they can fit in standard engine vehicles and require similar refueling times.

I first wrote about the Cummins B 6.7H engines in Cummins Shows Hydrogen Internal Combustion-Engined Concept Truck At IAA Transportation Exhibition, which I posted in September 2022.

I have these further thoughts.

Cummins B Series Engine

The Wikipedia entry for the Cummins B Series Engine, starts with these two paragraphs.

The Cummins B Series is a family of diesel engines produced by American manufacturer Cummins. In production since 1984, the B series engine family is intended for multiple applications on and off-highway, light-duty, and medium-duty. In the automotive industry, it is best known for its use in school buses, public service buses (most commonly the Dennis Dart and the Alexander Dennis Enviro400) in the United Kingdom, and Dodge/Ram pickup trucks.

Since its introduction, three generations of the B series engine have been produced, offered in both inline-four and inline-six configurations in multiple displacements.

Note.

- Cummins B Series is used in a wide variety of vehicles.

- It is available in both four and six cylinder versions.

But what Wikipedia doesn’t say, is that any Cummins’ customer will get the engine he wants for his application, even if it means creating a special version of the engine. Thirty years ago, I did a small data analysis job for Cummins in Darlington and on a tour of the works, I was given full details on how they treated customers. Cummins are not your average US company.

London’s Routemaster Buses

These buses are powered by a small four-cylinder version of the B-series engine, called a 4.5L ISB, which is described like this in Wikipedia.

The 4.5L ISB is essentially a four-cylinder, two-thirds version of the 6.7L ISB rated at 185 hp (138 kW), used in the New Routemaster, a series hybrid diesel-electric double-decker bus in London.

Note.

- Some diesel Range-Rovers, have more power, than these buses, but then they’re not hybrids.

- The engine also needs to be smaller, as it’s mounted under the back stairs.

Did Cummins’ special engine. allow the unique design of London’s Routemaster Buses?

Could London’s Routemaster Buses Be Converted To Hydrogen?

As an engineer and with my knowledge of Cummins’ design and manufacturing methods, I am fairly certain, if Cummins can manufacture six-cylinder versions of the B-Series engines, then four-cylinder hydrogen-powered engines are not far behind.

If London were to convert the thousand New Routemaster buses to hydrogen, there would be winners all round.

- Cummins would love the publicity and would probably benefit from increased sales of their hydrogen engines in vehicles like refuse trucks and small buses.

- It would surely give a route to convert older vehicles to hydrogen.

- The air in cities will improve.

But London has a problem, It is one of the few large cities in the world without readily-available hydrogen.

As this post illustrates and my Google searches show, India has a more advanced and scientifically-correct view on the usefulness of hydrogen.

Will Jaguar Land Rover Switch To Cummins’ Hydrogen Engines?

If Tata Motors make a success of hydrogen in India, it must make them think about adding hydrogen engines to Jaguar Land Rover products, specially as other manufacturers are getting serious about hydrogen.

Conclusion

Cummins will change the world for the better.

RWE And the Norfolk Wind Farms

In March 2024, I wrote RWE And Vattenfall Complete Multi-Gigawatt Offshore Wind Transaction In UK, which described how Vattenfall had sold 4.2 GW of offshore wind farms, situated off North-East Norfolk to RWE.

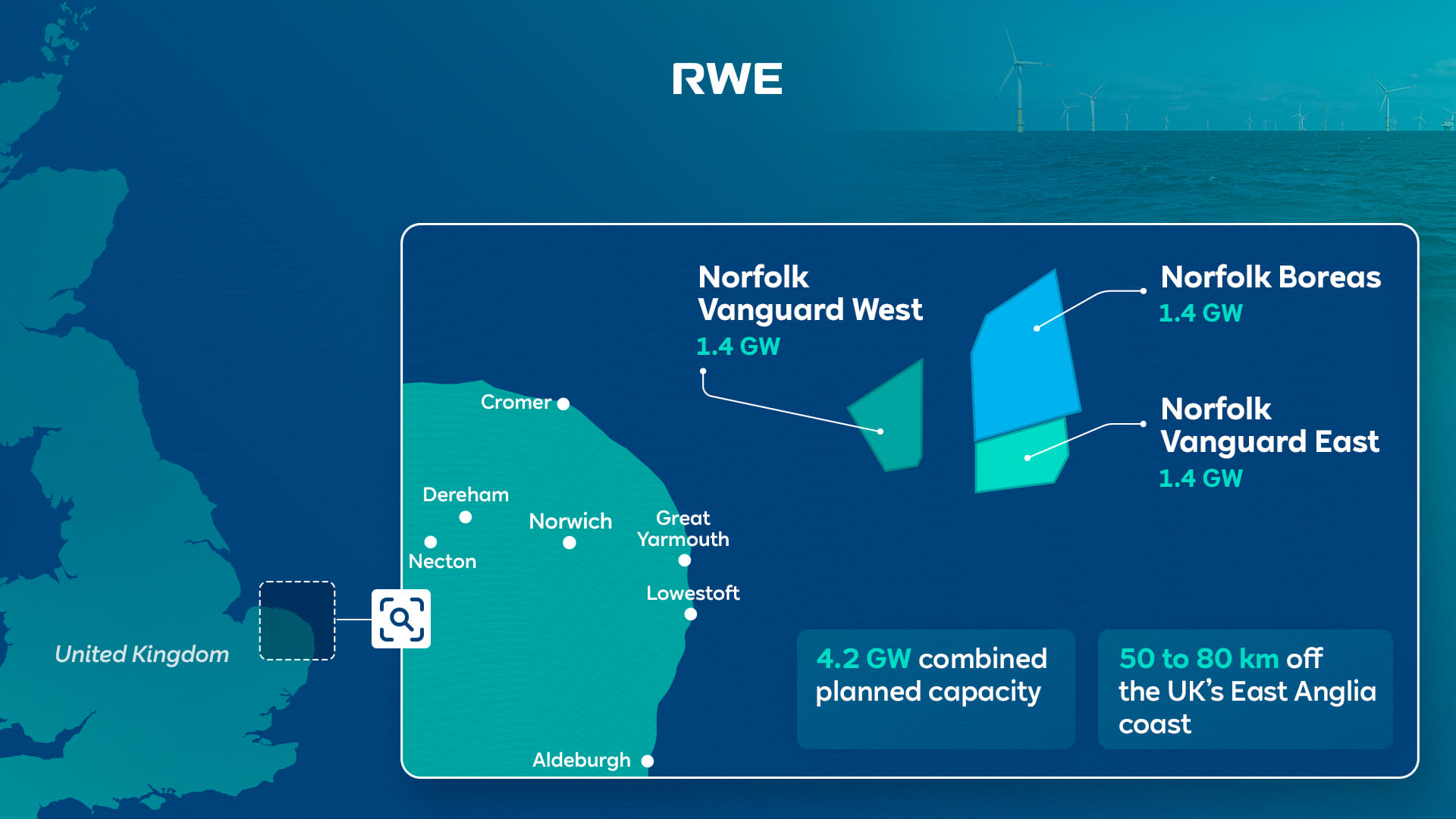

This map from RWE shows the wind farms.

Note.

- The Norfolk Zone consists of three wind farms; Norfolk Vanguard West, Norfolk Boreas and Norfolk Vanguard East.

- The three wind farms are 1.4 GW fixed-foundation wind farms.

- In Vattenfall Selects Norfolk Offshore Wind Zone O&M Base, I describe how the Port of Great Yarmouth had been selected as the O & M base.

- Great Yarmouth and nearby Lowestoft are both ports, with a long history of supporting shipbuilding and offshore engineering.

The wind farms and the operational port are all close together, which probably makes things convenient.

So why did Vattenfall sell the development rights of the three wind farms to RWE?

Too Much Wind?

East Anglia is fringed with wind farms all the way between the Wash and the Thames Estuary.

- Lincs – 270 MW

- Lynn and Inner Dowsing – 194 MW

- Race Bank – 580 MW

- Triton Knoll – 857 MW

- Sheringham Shoal – 317 MW

- Dudgeon – 402 MW

- Hornsea 3 – 2852 MW *

- Scroby Sands – 60 MW

- East Anglia One North – 800 MW *

- East Anglia Two – 900 MW *

- East Anglia Three – 1372 MW *

- Greater Gabbard – 504 MW

- Galloper – 353 MW

- Five Estuaries – 353 MW *

- North Falls – 504 MW *

- Gunfleet Sands – 172 MW

- London Array – 630 MW

Note.

- Wind farms marked with an * are under development or under construction.

- There is 4339 MW of operational wind farms between the Wash and the Thames Estuary.

- An extra 6781 MW is also under development.

If all goes well, East Anglia will have over 11 GW of operational wind farms or over 15 GW, if the three Norfolk wind farms are built.

East Anglia is noted more for its agriculture and not for its heavy industries consuming large amounts of electricity, so did Vattenfall decide, that there would be difficulties selling the electricity?

East Anglia’s Nimbies

East Anglia’s Nimbies seem to have started a campaign against new overground cables and all these new wind farms will need a large capacity increase between the main substations of the National Grid and the coast.

So did the extra costs of burying the cable make Vattenfall think twice about developing these wind farms?

East Anglia and Kent’s Interconnectors

East Anglia and Kent already has several interconnectors to Europe

- Viking Link – Bicker Fen and Jutland – 1.4 GW

- LionLink – Suffolk and the Netherlands – 1.8 GW – In Planning

- Nautilus – Suffolk or Isle of Grain and Belgium – 1.4 GW – In Planning

- BritNed – Isle of Grain and Maasvlakte – 1.0 GW

- NeuConnect – Isle of Grain and Wilhelmshaven – 1.4 GW – Under Construction

- GridLink Interconnector – Kingsnorth and Warande – 1.4 GW – Proposed

- HVDC Cross-Channel – Sellinge and Bonningues-lès-Calais – 2.0 GW

- ElecLink – Folkestone and Peuplingues – 1.0 GW

- Nemo Link – Richborough and Zeebrugge – 1.0 GW

Note.

- Five interconnectors with a capacity of 6.4 GW.

- A further four interconnectors with a capacity of 6 GW are on their way.

At 12.4 GW, the future capacity of the interconnectors between South-East England and Europe, is nor far short of South-East English wind power.

There are also two gas pipelines from the Bacton gas terminal between Cromer and Great Yarmouth to Europe.

The Wikipedia entry for the Bacton gas terminal gives these descriptions of the two gas pipelines.

Interconnector UK – This can import gas from, or export gas to, Zeebrugge, Belgium via a 235 km pipeline operating at up to 147 bar. There is a 30-inch direct access line from the SEAL pipeline. The Interconnector was commissioned in 1998.

BBL (Bacton–Balgzand line) – This receives gas from the compressor station in Anna Paulowna in the Netherlands. The BBL Pipeline is 235 km long and was commissioned in December 2006.

It would appear that East Anglia and Kent are well connected to the Benelux countries, with both electricity and gas links, but with the exception of the Viking Link, there is no connection to the Scandinavian countries.

Did this lack of connection to Sweden make convincing the Swedish government, reluctant to support Vattenfall in their plans?

Bringing The Energy From The Norfolk Wind Farms To Market

It looks to me, that distributing up to 4.2 GW from the Norfolk wind farms will not be a simple exercise.

- Other wind farms like the 2852 MW Hornsea 3 wind farm, may need a grid connection on the North Norfolk coast.

- The Nimbies will not like a South-Western route to the National Grid at the West of Norwich.

- An interconnector to Denmark or Germany from North Norfolk would probably help.

But at least there are two gas pipelines to Belgium and the Netherlands.

RWE, who now own the rights to the Norfolk wind farms, have a large amount of interests in the UK.

- RWE are the largest power producer in the UK.

- They supply 15 % of UK electricity.

- They have interest in twelve offshore wind farms in the UK. When fully-developed, they will have a capacity of almost 12 GW.

- RWE are developing the Pembroke Net Zero Centre, which includes a hydrogen electrolyser.

RWE expects to invest up to £15 billion in the UK by 2030 in new and existing green technologies and infrastructure as part of this.

Could this be RWE’s plan?

As the Norfolk wind farms are badly placed to provide electricity to the UK grid could RWE have decided to use the three Norfolk wind farms to produce hydrogen instead.

- The electrolyser could be placed onshore or offshore.

- If placed onshore, it could be placed near to the Bacton gas terminal.

- There are even depleted gas fields, where hydrogen could be stored.

How will the hydrogen be distributed and/or used?

It could be delivered by tanker ship or tanker truck to anyone who needs it.

In Developing A Rural Hydrogen Network, I describe how a rural hydrogen network could be developed, that decarbonises the countryside.

There are three major gas pipelines leading away from the Bacton gas terminal.

- The connection to the UK gas network.

- Interconnector UK to Belgium.

- BBL to The Netherlands.

These pipelines could be used to distribute hydrogen as a hydrogen blend with natural gas.

In UK – Hydrogen To Be Added To Britain’s Gas Supply By 2025, I describe the effects of adding hydrogen to the UK’s natural gas network.