Global Investor Joining RWE On Two Norfolk Vanguard Offshore Wind Projects, FID Expected in Summer

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

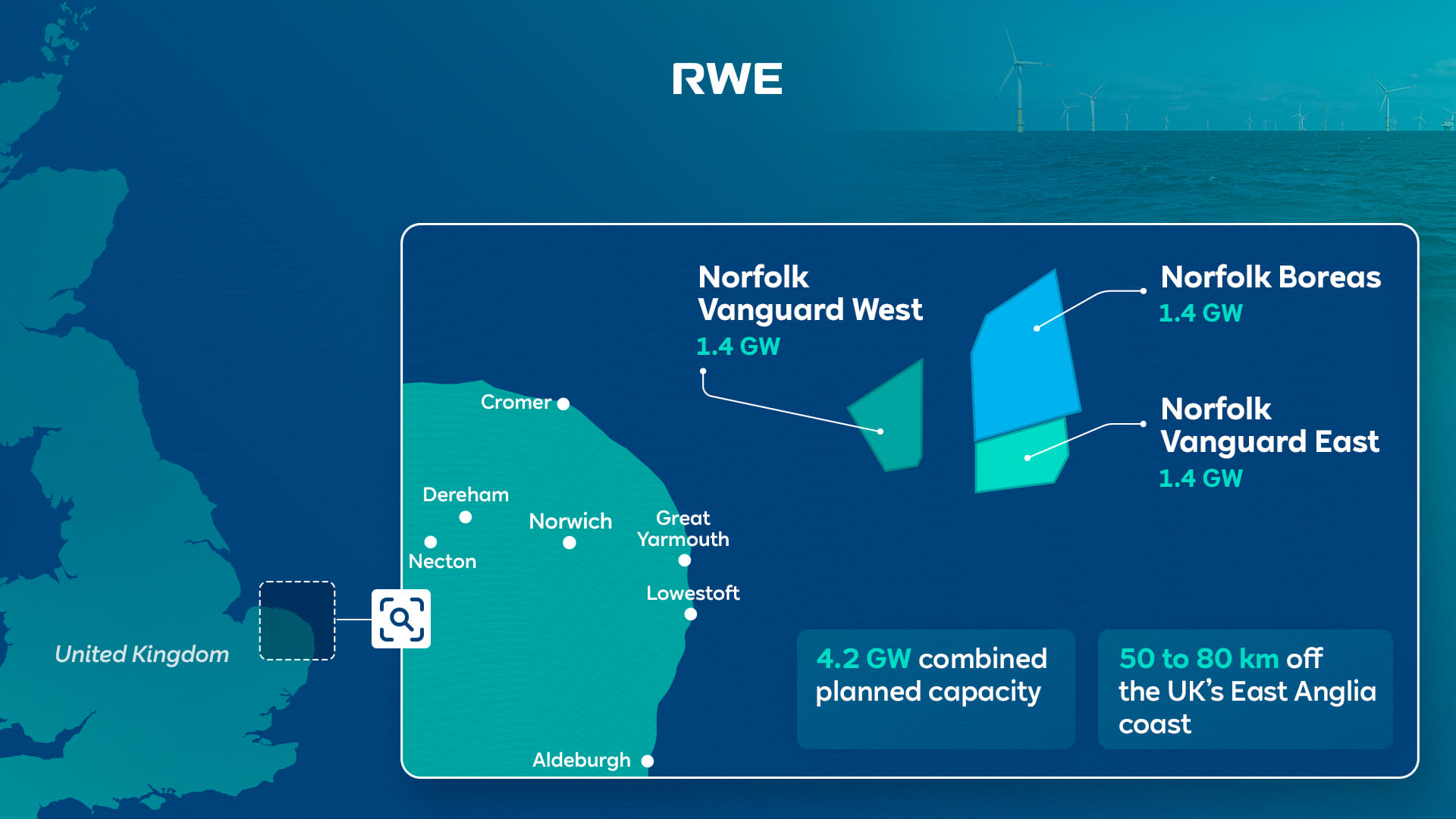

Global investment firm KKR and RWE have signed an agreement under which KKR acquire a 50 per cent stake in each of RWE’s Norfolk Vanguard East and Norfolk Vanguard West offshore wind projects, totalling 3.1 GW in installed capacity. The wind farms were just awarded Contracts for Difference (CfDs) in the UK’s seventh CfD allocation round (AR7).

These three paragraphs add a few more details.

The two Norfolk Vanguard projects, which RWE bought from Vattenfall in March 2024, have already secured seabed rights, grid connections, development consent orders (DCOs) and all other key permits.

On 14 January, RWE said it launched the process to raise non-recourse project finance debt for the projects and that it expects the closing of the partnership transaction and the project financing, as well as the final investment decision (FID), in the summer of 2026.

Located 50 to 80 kilometres off the coast of Norfolk, the two offshore wind farms are planned to be commissioned in 2029 (Norfolk Vanguard West) and 2030 (Norfolk Vanguard East).

RWE do seem to be lining up everything ready for that final investment decision in the summer of 2026.

- I suspect that with KKR on board, that they have got the money ready and I wouldn’t be surprised to see these two projects quickly progress to a completion.

- I also think it was significant that we have Goldman Sachs involved in Highview Power, who may have a solution to affordable energy storage and now we have KKR getting involved with one of the most professional offshore wind power developers in the world.

- Are Goldman Sachs and KKR placing bets against Trump’s anti wind power stance?

The Germans will certainly need a lot of energy and British offshore wind power, would appear the only place, where it is available easily in quantity to the Germans.

I await the next few months with a lot of interest.

Does Nuclear Power Not Sell Newspapers?

Five days ago, In Rolls-Royce SMR Advances To Final Stage In Swedish Nuclear Competition, I wrote about Rolls-Royce being one of two successful bids to advance to the ext stage to build Small Modular Reactors for Vatenfall in Sweden.

Since then, Rolls-Royce’s Swedish success has not featured in any newspaper in the UK, not even the Financial Times.

I can only assume, that good news stories about nuclear power, don’t sell newspapers.

Rolls-Royce SMR Advances To Final Stage In Swedish Nuclear Competition

The title of this post, is the same as that of this press release from Rolls-Royce.

This is the sub-heading.

Rolls-Royce SMR has been selected by Vattenfall as one of only two companies to reach the final stage in the process to identify Sweden’s nuclear technology partner.

These are the first two paragraphs, which add details.

After being shortlisted in 2024, Rolls-Royce SMR has progressed through a detailed assessment and will now work with Vattenfall through the final technology selection which could initially result in Rolls-Royce SMR delivering three SMRs.

This positive news is testament to Rolls-Royce SMR’s transformative approach to delivering proven nuclear technology in an innovative way through modularisation and builds on our successful selection in both the United Kingdom and Czech Republic.

Some other points from the press release.

- Sweden is initially looking to build three SMRs.

- Each SMR will supply 470MWe of clean low-carbon electricity.

- They are expected to have a lifetime of sixty years. Sizewell B was originally expected to have a lifetime of forty years, but appears to be being extended to sixty years, so I will accept Rolls-Royce’s expected lifetime.

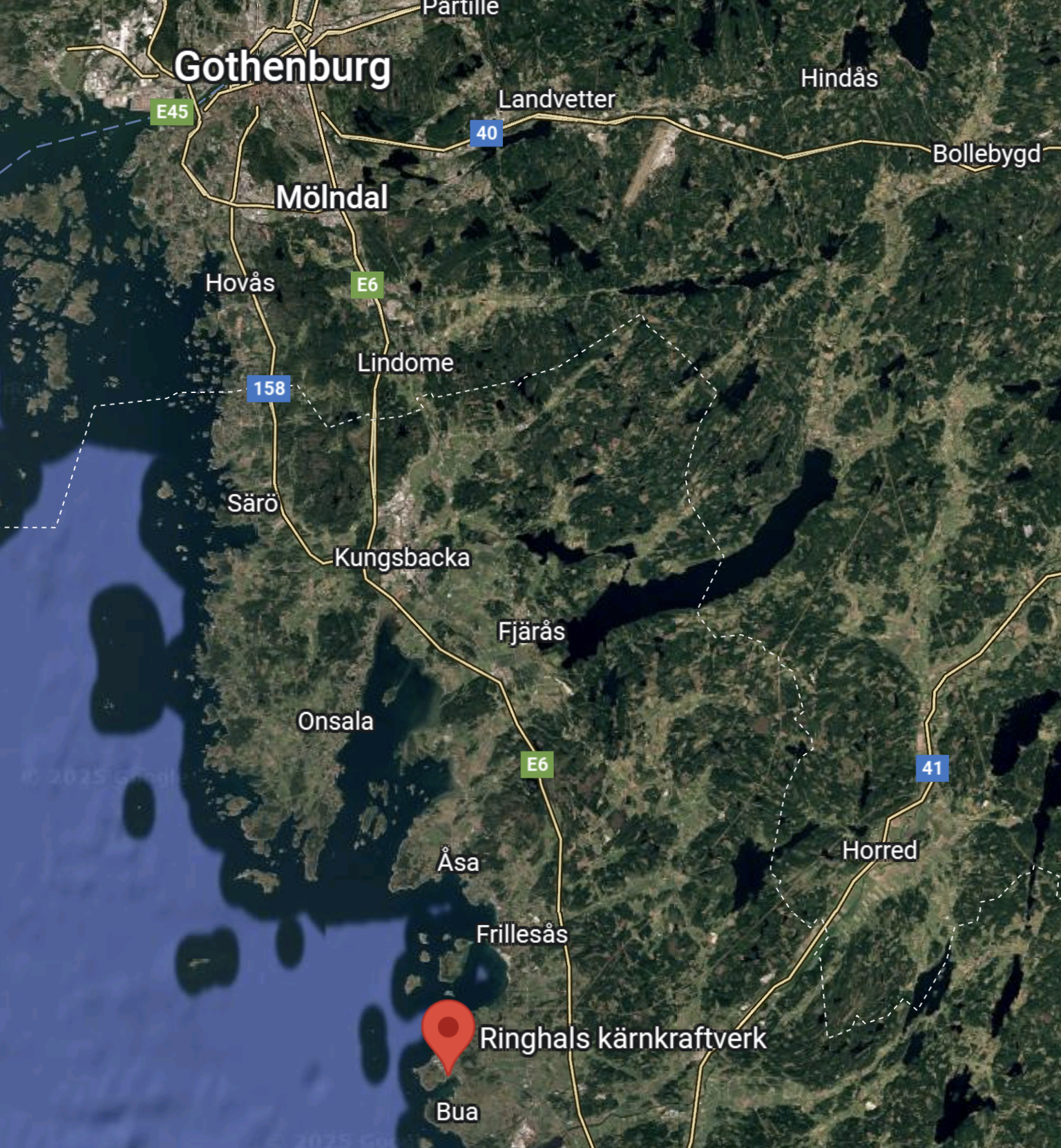

- The first units will be at the Ringhals site on the Värö Peninsula, where there is an existing nuclear power station.

This Google Map shows the Ringhals site in relation to Gothenburg.

The site is marked by the red arrow.

On taking a closer look, it appears to be a site with expansion possibilities.

The British Media Don’t Seem Very Interested

It is now the 31st of August and the only paper to report the story has been the Financial Times.

First Commercial-Scale Seaweed Farm Between Wind Turbines Fully Operational In Netherlands

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

The world’s first commercial-scale seaweed farm within the Hollandse Kust Zuid offshore wind farm in the Netherlands is fully operational.

These initial three paragraphs fill out the details.

According to the non-profit organisation North Sea Farmers (NSF), the final deployment step was completed one week ago by deploying the seeded substrate.

North Sea Farm 1, initiated by NSF with funding from Amazon’s Right Now Climate Fund, is a floating farm located in the open space between wind turbines where seaweed production can be tested and improved.

The seaweed farm is located within the Hollandse Kust Zuid wind farm, nearly 22 kilometres off the coast of Scheveningen. The 1.5 GW project is owned by Vattenfall, BASF, and Allianz.

I find this an interesting concept.

I can remember reading in the Meccano Magazine in the 1950s, about the production of alginates from seaweed in Scotland.

Surprisingly, Wikipedia has very little on alginates, except for this illuminating Wikipedia entry for alginic acid.

This is the opening paragraph.

Alginic acid, also called algin, is a naturally occurring, edible polysaccharide found in brown algae. It is hydrophilic and forms a viscous gum when hydrated. When the alginic acid binds with sodium and calcium ions, the resulting salts are known as alginates. Its colour ranges from white to yellowish-brown. It is sold in filamentous, granular, or powdered forms.

But it does appear that the Scottish production of alginates is very much of the past. Unless someone else can enlighten me!

Perhaps Scottish seaweed farming can be revived to produce alginates, which appear to have a surprising number of uses, as this section of the Wikipedia entry shows.

Alginates do appear to be remarkably useful.

These are a few uses.

- As of 2022 alginate had become one of the most preferred materials as an abundant natural biopolymer.

- Sodium alginate is mixed with soybean protein to make meat analogue.

- They are an ingredient of Gaviscon and other pharmaceuticals.

- Sodium alginate is used as an impression-making material in dentistry, prosthetics, lifecasting, and for creating positives for small-scale casting.

- Sodium alginate is used in reactive dye printing and as a thickener for reactive dyes in textile screen-printing.

- Calcium alginate is used in different types of medical products, including skin wound dressings to promote healing,

Alginates seem to have some rather useful properties.

Four years ago, I tripped over in my bedroom, which I wrote about in An Accident In My Bedroom. I wonder if the Royal London Hospital used calcium alginate skin dressings to restore my hand to its current condition.

Paul Daniels would have said, “It’s magic!”

In the future these dressings may be produced from UK-produced seaweed.

H2ercules

H2ercules is a project that will create the German hydrogen network.

The H2ercules web site, introduces the project with these two paragraphs.

A faster ramp-up of the hydrogen economy in Germany is more important than ever in order to drive forward the decarbonisation programme, put the German energy system on a more robust footing, and thus contribute towards a green security of supply. What this needs is a geographical realignment of the infrastructure for energy in gas form: Instead of flowing from the east of Germany to the west and south of the country, the gas – natural gas now, hydrogen in the future – will have to make its way in future from generation locations in the north-west to centres of consumption located mainly in the west and south. That also means that new sources will have to be connected, and gaps in existing pipeline networks will have to be closed. To speed up this vital process, OGE and RWE have developed the national infrastructure project “H2ercules”, which is intended to supply consumers in Germany’s south and west with domestically produced green hydrogen from the north of the country, in addition to imported sources. This will involve connecting up the electrolyser capacities that are currently being planned and developing more besides. RWE wants to create up to 1 GW of additional electrolyser capacity as part of the H2ercules project. For the connection component, OGE is planning to put 1,500 km of pipelines in place. For the most part, this will mean converting pipelines from the existing natural gas network to hydrogen, supplemented by newly constructed facilities. Converting natural gas pipelines is not only the more cost-efficient solution, but it also allows for a faster schedule. The system is expected to be supplemented by the planned hydrogen storages of RWE.

The current plan is to complete the project in three stages between 2026 and 2030, in order to connect industries to the hydrogen supply as soon as possible. The aim of this collaboration across multiple value levels is to resolve the chicken-and-egg problem on a super-sized scale and also smooth the way forward for other projects.

Note.

There will be a lot of conversion of the existing natural gas network to hydrogen.

RWE wants to create up to 1 GW of additional electrolyser capacity as part of the H2ercules project.

The second paragraph indicates to me, that they want to move fast.

This map from the H2ercules web site, indicate the proposed size of the network in 2030.

These three paragraphs describe how H2ercules will be developed.

OGE and RWE are both strong companies that aim to combine forces as part of the H2ercules project in order to overcome this Herculean task. While the task for OGE will be to convert the required gas pipelines to hydrogen and construct new pipelines, RWE will expand its electrolyser capacity and import green hydrogen in addition. Gas-fired power stations with a capacity of at least 2 GW will be converted to hydrogen, and new H2 -storages as well as H2-storages repurposed from gas storages on the Dutch border will be connected to the hydrogen supply system.

H2ercules also opens up new opportunities to connect Germany’s future centres of hydrogen consumption to key import routes, first via pipelines from Belgium and the Netherlands, and later via Norway and also from southern and eastern Europe, with the added prospects of import terminals for green molecules in Germany’s north. The project is thus contributing significantly to the creation of a European hydrogen market.

The first additional companies and organisations have already indicated their interest in this project, and it is expected that in the future smaller businesses will benefit in addition to large-scale customers, as the entire industry is guided towards a decarbonised future.

These are my thoughts.

Why Is It Called H2ercules?

I suspect, it’s nothing more, than the Germans wanted a recognisable and catchy name.

- Name selection is not helped by the German for hydrogen, which is wasserstoff.

- Hercules is Herkules in German, which doesn’t really help.

- Projekt Wasserstoff isn’t as memorable as H2ercules, which at least isn’t English.

It looks to me, that the Germans have come up with a good acceptable compromise.

The Wilhemshaven Hydrogen Import Terminal

German energy company; Uniper is building a hydrogen import terminal at Wilhemshaven to feed H2ercules and German industry with hydrogen from places like Australia, Namibia and the Middle East. I wrote about this hydrogen import terminal in Uniper To Make Wilhelmshaven German Hub For Green Hydrogen; Green Ammonia Import Terminal.

Wilhelmshaven and Great Yarmouth are 272 miles or 438 kilometres apart, so a pipeline or a tanker link would be feasible to export hydrogen from Notfolk to Germany.

I suspect RWE will build a giant offshore electrolyser close to the Norfolk wind farms and the hydrogen will be exported by tanker or pipeline to Germany or to anybody else who pays the right price.

RWE’s Norfolk Wind Farms

What is interesting me, is what Germany company; RWE is up to. Note they are one of the largest UK electricity producers.

In December 2023, they probably paid a low price, for the rights for 3 x 1.4 GW wind farms about 50 km off North-East Norfolk from in-trouble Swedish company; Vattenfall and have signed contracts to build them fairly fast.

In March 2024, I wrote about the purchase in RWE And Vattenfall Complete Multi-Gigawatt Offshore Wind Transaction In UK.

This map from RWE shows the three wind farms, with respect to the Norfolk coast.

Could it be, that RWE intend to build a giant offshore electrolyser to the East of Great Yarmouth?

- The planning permission for an electrolyser, which is eighty kilometres offshore, would be far easier, than for one onshore.

- The hydrogen pipeline between Norfolk and Germany would be less than 400 kilometres.

- Hydrogen could also be brought ashore in Norfolk, if the price was right.

- The Bacton gas terminal is only a few miles North of Great Yarmouth.

But the big advantage, is that the only onshore construction could be restricted to the Bacton gas terminal.

Adding More Wind Farms To The Electrolyser

Looking at the RWE map, the following should be noted.

South of Norfolk Vanguard East, there is the East Anglian Array wind farm, which by the end of 2026, will consist of these wind farms.

- East Anglia One – 714 MW – 2020

- East Anglia One North – 800 MW – 2026

- East Anglia Two – 900 MW – 2026

- East Anglia Three – 1372 MW – 2026

Note.

- The date is the commissioning date.

- There is a total capacity of 3786 MW

- All wind farms are owned by Iberdrola.

- There may be space to add other sections to the East Anglian Array.

I doubt, it would be difficult for some of Iberdrola’s megawatts to be used to generate hydrogen for Germany.

To the East of Norfolk Boreas and Norfolk Vanguard East, it’s Dutch waters, so I doubt the Norfolk cluster can expand to the East.

But looking at this map of wind farms, I suspect that around 4-5 GW of new wind farms could be squeezed in to the North-West of the the Norfolk Cluster and South of the Hornsea wind farms.

The 1.5 GW Outer Dowsing wind farm, which is being planned, will be in this area.

I can certainly see 8-10 GW of green electricity capacity being available to electrolysers to the North-East of Great Yarmouth.

Conclusion

UK offshore electricity could be the power behind H2ercules.

- The hydrogen could be sent to Germany by pipeline or tanker ship, as the distance is under 400 kilometers to the Wilhelmshaven hydrogen hub.

- Extra electrolysers and wind farms could be added as needed.

- The hydrogen won’t need to be shipped halfway round the world.

The cash flow won’t hurt the UK.

.

Do RWE Have A Comprehensive Hydrogen Plan For Germany?

What is interesting me, is what Germany company; RWE is up to. They are one of the largest UK electricity producers.

In December 2023, they probably paid a low price, for the rights for 3 x 1.4 GW wind farms about 50 km off North-East Norfolk from in-trouble Swedish company; Vattenfall and have signed contracts to build them fairly fast.

In March 2024, wrote about the purchase in RWE And Vattenfall Complete Multi-Gigawatt Offshore Wind Transaction In UK.

Over the last couple of years, I have written several posts about these three wind farms.

March 2023 – Vattenfall Selects Norfolk Offshore Wind Zone O&M Base

November 2023 – Aker Solutions Gets Vattenfall Nod To Start Norfolk Vanguard West Offshore Platform

December 2023 – SeAH To Deliver Monopiles For Vattenfall’s 2.8 GW Norfolk Vanguard Offshore Wind Project

Then in July 2023, I wrote Vattenfall Stops Developing Major Wind Farm Offshore UK, Will Review Entire 4.2 GW Zone

Note.

- There does appear to be a bit of a mix-up at Vattenfall, judging by the dates of the reports.Only, one wind farm has a Contract for Difference.

- It is expected that the other two will be awarded contracts in Round 6, which should be by Summer 2024.

In December 2023, I then wrote RWE Acquires 4.2-Gigawatt UK Offshore Wind Development Portfolio From Vattenfall.

It appears that RWE paid £963 million for the three wind farms.

I suspect too, they paid for all the work Vattenfall had done.

This transaction will give RWE 4.2 GW of electricity in an area with very bad connections to the National Grid and the Norfolk Nimbies will fight the building of more pylons.

So have the Germans bought a pup?

I don’t think so!

Where Is Wilhemshaven?

This Google Map shows the location of Wilhemshaven.

Note.

- Heligoland is the island at the top of the map.

- The Germans call this area the Wdden Sea.

- The estuaries lead to Wilhelmshaven and Bremerhaven.

- Cuxhaven is the port for Heligoland, which is connected to Hamburg by hydrogen trains.

This second map shows between Bremerhaven and Wilhelmshaven.

Note.

- Wilhelmshaven is to the West.

- Bremerhaven is in the East.

- The River Weser runs North-South past Bremerhaven.

I’ve explored the area by both car and train and it is certainly worth a visit.

The Wilhemshaven Hydrogen Import Terminal

German energy company; Uniper is building a hydrogen import terminal at Wilhemshaven to feed German industry with hydrogen from places like Australia, Namibia and the Middle East. I wrote about this hydrogen import terminal in Uniper To Make Wilhelmshaven German Hub For Green Hydrogen; Green Ammonia Import Terminal.

I suspect RWE could build a giant offshore electrolyser close to the Norfolk wind farms and the hydrogen will be exported by tanker or pipeline to Germany or to anybody else who pays the right price.

All this infrastructure will be installed and serviced from Great Yarmouth, so we’re not out of the deal.

Dogger Bank South Wind Farm

To make matters better, RWE have also signed to develop the 3 GW Dogger Bank South wind farm.

This could have another giant electrolyser to feed German companies. The wind farm will not need an electricity connection to the shore.

The Germans appear to be taking the hydrogen route to bringing electricity ashore.

Energy Security

Surely, a short trip across the North Sea, rather than a long trip from Australia will be much more secure and on my many trips between the Haven Ports and The Netherlands, I haven’t yet seen any armed Houthi pirates.

RWE And Hydrogen

On this page on their web site, RWE has a lot on hydrogen.

Very Interesting!

H2ercules

This web site describes H2ercules.

The goal of the H2ercules initiative is to create the heart of a super-sized hydrogen infrastructure for Germany by 2030. To make this happen, RWE, OGE and, prospectively, other partners are working across various steps of the value chain to enable a swift supply of hydrogen from the north of Germany to consumers in the southern and western areas of the country. In addition to producing hydrogen at a gigawatt scale, the plan is also to open up import routes for green hydrogen. The transport process will involve a pipeline network of about 1,500 km, most of which will consist of converted gas pipelines.

Where’s the UK’s H2ercules?

Conclusion

The Germans have got there first and will be buying up all of our hydrogen to feed H2ercules.

RWE And the Norfolk Wind Farms

In March 2024, I wrote RWE And Vattenfall Complete Multi-Gigawatt Offshore Wind Transaction In UK, which described how Vattenfall had sold 4.2 GW of offshore wind farms, situated off North-East Norfolk to RWE.

This map from RWE shows the wind farms.

Note.

- The Norfolk Zone consists of three wind farms; Norfolk Vanguard West, Norfolk Boreas and Norfolk Vanguard East.

- The three wind farms are 1.4 GW fixed-foundation wind farms.

- In Vattenfall Selects Norfolk Offshore Wind Zone O&M Base, I describe how the Port of Great Yarmouth had been selected as the O & M base.

- Great Yarmouth and nearby Lowestoft are both ports, with a long history of supporting shipbuilding and offshore engineering.

The wind farms and the operational port are all close together, which probably makes things convenient.

So why did Vattenfall sell the development rights of the three wind farms to RWE?

Too Much Wind?

East Anglia is fringed with wind farms all the way between the Wash and the Thames Estuary.

- Lincs – 270 MW

- Lynn and Inner Dowsing – 194 MW

- Race Bank – 580 MW

- Triton Knoll – 857 MW

- Sheringham Shoal – 317 MW

- Dudgeon – 402 MW

- Hornsea 3 – 2852 MW *

- Scroby Sands – 60 MW

- East Anglia One North – 800 MW *

- East Anglia Two – 900 MW *

- East Anglia Three – 1372 MW *

- Greater Gabbard – 504 MW

- Galloper – 353 MW

- Five Estuaries – 353 MW *

- North Falls – 504 MW *

- Gunfleet Sands – 172 MW

- London Array – 630 MW

Note.

- Wind farms marked with an * are under development or under construction.

- There is 4339 MW of operational wind farms between the Wash and the Thames Estuary.

- An extra 6781 MW is also under development.

If all goes well, East Anglia will have over 11 GW of operational wind farms or over 15 GW, if the three Norfolk wind farms are built.

East Anglia is noted more for its agriculture and not for its heavy industries consuming large amounts of electricity, so did Vattenfall decide, that there would be difficulties selling the electricity?

East Anglia’s Nimbies

East Anglia’s Nimbies seem to have started a campaign against new overground cables and all these new wind farms will need a large capacity increase between the main substations of the National Grid and the coast.

So did the extra costs of burying the cable make Vattenfall think twice about developing these wind farms?

East Anglia and Kent’s Interconnectors

East Anglia and Kent already has several interconnectors to Europe

- Viking Link – Bicker Fen and Jutland – 1.4 GW

- LionLink – Suffolk and the Netherlands – 1.8 GW – In Planning

- Nautilus – Suffolk or Isle of Grain and Belgium – 1.4 GW – In Planning

- BritNed – Isle of Grain and Maasvlakte – 1.0 GW

- NeuConnect – Isle of Grain and Wilhelmshaven – 1.4 GW – Under Construction

- GridLink Interconnector – Kingsnorth and Warande – 1.4 GW – Proposed

- HVDC Cross-Channel – Sellinge and Bonningues-lès-Calais – 2.0 GW

- ElecLink – Folkestone and Peuplingues – 1.0 GW

- Nemo Link – Richborough and Zeebrugge – 1.0 GW

Note.

- Five interconnectors with a capacity of 6.4 GW.

- A further four interconnectors with a capacity of 6 GW are on their way.

At 12.4 GW, the future capacity of the interconnectors between South-East England and Europe, is nor far short of South-East English wind power.

There are also two gas pipelines from the Bacton gas terminal between Cromer and Great Yarmouth to Europe.

The Wikipedia entry for the Bacton gas terminal gives these descriptions of the two gas pipelines.

Interconnector UK – This can import gas from, or export gas to, Zeebrugge, Belgium via a 235 km pipeline operating at up to 147 bar. There is a 30-inch direct access line from the SEAL pipeline. The Interconnector was commissioned in 1998.

BBL (Bacton–Balgzand line) – This receives gas from the compressor station in Anna Paulowna in the Netherlands. The BBL Pipeline is 235 km long and was commissioned in December 2006.

It would appear that East Anglia and Kent are well connected to the Benelux countries, with both electricity and gas links, but with the exception of the Viking Link, there is no connection to the Scandinavian countries.

Did this lack of connection to Sweden make convincing the Swedish government, reluctant to support Vattenfall in their plans?

Bringing The Energy From The Norfolk Wind Farms To Market

It looks to me, that distributing up to 4.2 GW from the Norfolk wind farms will not be a simple exercise.

- Other wind farms like the 2852 MW Hornsea 3 wind farm, may need a grid connection on the North Norfolk coast.

- The Nimbies will not like a South-Western route to the National Grid at the West of Norwich.

- An interconnector to Denmark or Germany from North Norfolk would probably help.

But at least there are two gas pipelines to Belgium and the Netherlands.

RWE, who now own the rights to the Norfolk wind farms, have a large amount of interests in the UK.

- RWE are the largest power producer in the UK.

- They supply 15 % of UK electricity.

- They have interest in twelve offshore wind farms in the UK. When fully-developed, they will have a capacity of almost 12 GW.

- RWE are developing the Pembroke Net Zero Centre, which includes a hydrogen electrolyser.

RWE expects to invest up to £15 billion in the UK by 2030 in new and existing green technologies and infrastructure as part of this.

Could this be RWE’s plan?

As the Norfolk wind farms are badly placed to provide electricity to the UK grid could RWE have decided to use the three Norfolk wind farms to produce hydrogen instead.

- The electrolyser could be placed onshore or offshore.

- If placed onshore, it could be placed near to the Bacton gas terminal.

- There are even depleted gas fields, where hydrogen could be stored.

How will the hydrogen be distributed and/or used?

It could be delivered by tanker ship or tanker truck to anyone who needs it.

In Developing A Rural Hydrogen Network, I describe how a rural hydrogen network could be developed, that decarbonises the countryside.

There are three major gas pipelines leading away from the Bacton gas terminal.

- The connection to the UK gas network.

- Interconnector UK to Belgium.

- BBL to The Netherlands.

These pipelines could be used to distribute hydrogen as a hydrogen blend with natural gas.

In UK – Hydrogen To Be Added To Britain’s Gas Supply By 2025, I describe the effects of adding hydrogen to the UK’s natural gas network.

RWE And Vattenfall Complete Multi-Gigawatt Offshore Wind Transaction In UK

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

RWE and Vattenfall have completed the sale of three offshore wind projects in the UK. With the transaction completed, RWE has expanded its offshore wind portfolio in the UK by 4.2 GW.

There is also this RWE infographic, which shows the three wind farms in relation to the East Anglian coast.

RWE are getting to be a big player in UK offshore wind, with these wind farm in operation or planned.

- Galloper – 353 MW – Operation

- Gwynt y Môr – 576 MW – Operation

- Rhyll Flats – 90 MW – Operation

- Triton Knoll – 857 MW – Operation

- Sofia – 1400 MW – Under Construction – Completion in 2026

- Norfolk Boreas – 1380 MW – Planned – Completion in 2027

- Norfolk Vanguard East – 1380 MW – Planned – Completion before 2030

- Norfolk Vanguard West – 1380 MW – Planned – Completion before 2030

- Dogger Bank South – 3000 MW – Planned

- Awel y Môr – 500 MW – Planned

- Five Estuaries – 353 MW – Planned

- North Falls – 504 MW – Planned

That is a total of 11,773 MW, of which 10,607 MW is on the German side of the UK.

With RWE likely to have some success in auctions this year, these figures, are likely to increase and some wind farms will start construction.

Enabling The UK To Become The Saudi Arabia Of Wind?

The title of this post, is the same as that of a paper from Imperial College.

The paper can be downloaded from this page of the Imperial College web site.

This is a paragraph from the Introduction of the paper.

In December 2020, the then Prime Minister outlined the government’s ten-point plan for a green industrial revolution, expressing an ambition “to turn the UK into the Saudi Arabia of wind power generation, enough wind power by 2030 to supply every single one of our homes with electricity”.

The reference to Saudi Arabia, one of the world’s largest oil producers for many decades, hints at the significant role the UK’s energy ambitions hoped to play in the global economy.

Boris Johnson was the UK Prime Minister at the time, so was his statement just his usual bluster or a simple deduction from the facts.

The paper I have indicated is a must-read and I do wonder if one of Boris’s advisors had read the paper before Boris’s speech. But as the paper appears to have been published in September 2023, that is not a valid scenario.

The paper though is full of important information.

The Intermittency Of Wind And Solar Power

The paper says this about the intermittency of wind and solar power.

One of the main issues is the intermittency of solar and wind electricity generation, which means it cannot be relied upon without some form of backup or sufficient storage.

Solar PV production varies strongly along both the day-night and seasonal cycles. While output is higher during the daytime (when demand is

higher than overnight), it is close to zero when it is needed most, during the times of peak electricity demand (winter evenings from 5-6 PM).At present, when wind output is low, the UK can fall back to fossil fuels to make up for the shortfall in electricity supply. Homes stay warm, and cars keep moving.

If all sectors were to run on variable renewables, either the country needs to curb energy usage during shortfalls (unlikely to be popular with consumers), accept continued use of fossil fuels across all sectors (incompatible with climate targets), or develop a large source of flexibility such as energy storage (likely to be prohibitively expensive at present).

The intermittency of wind and solar power means we have a difficult choice to make.

The Demand In Winter

The paper says this about the demand in winter.

There are issues around the high peaks in heating demand during winter, with all-electric heating very expensive to serve (as

the generators built to serve that load are only

needed for a few days a year).Converting all the UK’s vehicles to EVs would increase total electricity demand from 279 TWh to 395 TWh. Switching all homes across the country to heat pumps would increase demand by a further 30% to 506 TWh.

This implies that the full electrification of the heating and transport sectors would increase the annual power needs in the country by 81%.

This will require the expansion of the electricity system (transmission capacity, distribution grids, transformers,

substations, etc.), which would pose serious social, economic and technical challenges.Various paths, policies and technologies for the decarbonisation of heating, transport, and industrial emissions must be considered in order for the UK to meet its zero-emission targets.

It appears that electrification alone will not keep us warm, power our transport and keep our industry operating.

The Role Of Hydrogen

The paper says this about the role of hydrogen.

Electrifying all forms of transport might prove difficult (e.g., long-distance heavy goods) or nigh impossible (e.g., aviation) due to the high energy density requirements, which current batteries cannot meet.

Hydrogen has therefore been widely suggested as a low-carbon energy source for these sectors, benefiting from high energy density (by weight), ease of storage (relative to electricity) and its versatility to be used in many ways.

Hydrogen is also one of the few technologies capable of

providing very long-duration energy storage (e.g., moving energy between seasons), which is critical to supporting the decarbonisation of the whole energy system with high shares of renewables because it allows times of supply and demand mismatch to be managed over both short and long timescales.It is a clean alternative to fossil fuels as its use (e.g., combustion) does not emit any CO2.

Hydrogen appears to be ideal for difficult to decarbonise sectors and for storing energy for long durations.

The Problems With Hydrogen

The paper says this about the problems with hydrogen.

The growth of green hydrogen technology has been held back by the high cost, lack of existing infrastructure, and its lower efficiency

of conversion.Providing services with hydrogen requires two to three times more primary energy than direct use of electricity.

There is a lot of development to be done before hydrogen is as convenient and affordable as electricity and natural gas.

Offshore Wind

The paper says this about offshore wind.

Offshore wind is one of the fastest-growing forms of renewable energy, with the UK taking a strong lead on the global stage.

Deploying wind turbines offshore typically leads to a higher electricity output per turbine, as there are typically higher wind speeds and fewer obstacles to obstruct wind flow (such as trees and buildings).

The productivity of the UK’s offshore wind farms is nearly 50% higher than that of onshore wind farms.

Offshore wind generation also typically has higher social acceptability as it avoids land usage conflicts and has a lower visual impact.

To get the most out of this resource, very large structures (more than twice the height of Big Ben) must be connected to the ocean floor and operate in the harshest conditions for decades.

Offshore wind turbines are taller and have larger rotor diameters than onshore wind turbines, which produces a more consistent and higher output.

Offshore wind would appear to be more efficient and better value than onshore.

The Scale Of Offshore Wind

The paper says this about the scale of offshore wind.

The geographical distribution of offshore wind is heavily skewed towards Europe, which hosts over 80% of the total global offshore wind capacity.

This can be attributed to the good wind conditions and the shallow water depths of the North Sea.

The UK is ideally located to take advantage of offshore wind due to its extensive resource.

The UK could produce over 6000 TWh of electricity if the offshore wind resources in all the feasible area of the exclusive economic zone (EEZ) is exploited.

Note.

- 6000 TWh of electricity per annum would need 2740 GW of wind farms if the average capacity factor was a typical 25 %.

- At a price of 37.35 £/MWh, 6000 TWh would be worth $224.1 billion.

Typically, most domestic users seem to pay about 30 pence per KWh.

The Cost Of Offshore Wind

The paper says this about the cost of offshore wind.

The cost of UK offshore wind has fallen because of the reductions in capital expenditure (CapEx), operational expenditure (OpEx), and financing costs.

This has been supported by the global roll-out of bigger offshore wind turbines, hence, causing an increase in offshore wind energy capacity.

This increase in installed capacity has been fuelled by several low-carbon support schemes from the UK government.

The effect of these schemes can be seen in the UK 2017 Contracts for Difference (CfD) auctions where offshore wind reached strike prices as low as 57.50 £/MWh and an even lower strike price of 37.35 £/MWh in 2022.

Costs and prices appear to be going the right way.

The UK’s Offshore Wind Targets

The paper says this about the UK’s offshore wind targets.

The offshore wind capacity in the UK has grown over the past decade.

Currently, the UK has a total offshore wind capacity of 13.8GW, which is sufficient to power more than 10 million homes.

This represents a more than fourfold increase compared to the capacity installed in 2012.

The UK government has set ambitious targets for offshore wind development.

In 2019, the target was to install a total of 40 GW of offshore wind capacity by 2030, and this was later raised to 50 GW, with up to 5 GW of floating offshore wind.

This will play a pivotal role in decarbonising the UK’s power system by the government’s deadline of 2035.

As I write this, the UK’s total electricity production is 31.8 GW. So 50 GW of wind will go a good way to providing the UK with zero-carbon energy. But it will need a certain amount of reliable alternative power sources for when the wind isn’t blowing.

The UK’s Hydrogen Targets

The paper says this about the UK’s hydrogen targets.

The UK has a target of 10 GW of low-carbon hydrogen production to be deployed by 2030, as set out in the British Energy Security Strategy.

Within this target, there is an ambition for at least half of the 10 GW of production capacity to be met through green hydrogen production technologies (as opposed to hydrogen produced from steam methane reforming using carbon capture).

Modelling conducted by the Committee on Climate Change in its Sixth Carbon Budget estimated that demand for low-carbon hydrogen across the whole country could reach 161–376 TWh annually by 2050, comparable in scale to the total electricity demand.

We’re going to need a lot of electrolyser capacity.

Pairing Hydrogen And Offshore Wind

The paper says this about pairing hydrogen and offshore wind.

Green hydrogen holds strong potential in addressing the intermittent nature of renewable generation sources, particularly wind and solar energy, which naturally fluctuate due to weather conditions.

Offshore wind in particular is viewed as being a complementary technology to pair with green hydrogen production, due to three main factors: a) the high wind energy capacity factors offshore, b) the potential for large-scale deployment and c) hydrogen as a supporting technology for offshore wind energy integration.

It looks like a match made in the waters around the UK.

The Cost Of Green Hydrogen

The paper says this about the cost of green hydrogen.

The cost of green hydrogen is strongly influenced by the price of the electrolyser unit itself.

If the electrolyser is run more intensively over the course of the lifetime of the plant, a larger volume of hydrogen will be produced and so the cost of the electrolyser will be spread out more, decreasing the cost per unit of produced hydrogen.

If the variable renewable electricity source powering the electrolyser has a higher capacity factor, this will contribute towards a

lower cost of hydrogen produced.Offshore wind in the UK typically has a higher capacity factor than onshore wind energy (up to 20%), and is around five times higher than solar, so pairing

offshore wind with green hydrogen production is of interest.

It would appear that any improvements in wind turbine and electrolyser efficiency would be welcomed.

The Size Of Wind Farms

The paper says this about the size of wind farms.

Offshore wind farms can also be larger scale, due to increased availability of space and reduced restrictions on tip heights due to planning permissions.

The average offshore wind turbine in the UK had a capacity of 3.6 MW in 2022, compared to just 2.5-3 MW for onshore turbines.

As there are fewer competing uses for space, offshore wind can not only have larger turbines but the wind farms can comprise many more turbines.

Due to the specialist infrastructure requirements for hydrogen transport and storage, and the need for economies of scale to reduce the costs of

production, pairing large-scale offshore wind electricity generation with green hydrogen

production could hold significant benefits.

I am not surprised that economies of scale give benefits.

The Versatility Of Hydrogen

The paper says this about the versatility of hydrogen.

Hydrogen is a highly adaptable energy carrier with numerous potential applications and has been anticipated by some as playing a key role in the future energy system, especially when produced through electrolysis.

It could support the full decarbonisation of “hard to decarbonise” processes within the UK industrial sector, offering a solution for areas which may be difficult to electrify or are heavily reliant on fossil fuels for high-temperature heat.

When produced through electrolysis, it could be paired effectively as an energy storage technology with offshore wind, with the potential to store energy across seasons with little to no energy degradation and transport low-carbon energy internationally.

The UK – with its significant offshore wind energy resources and targets – could play a potentially leading role in producing green hydrogen to both help its pathway to net zero, and potentially create a valuable export industry.

In RWE Acquires 4.2-Gigawatt UK Offshore Wind Development Portfolio From Vattenfall, I postulated that RWE may have purchased Vattenfall’s 4.2 GW Norfolk Zone of windfarms to create a giant hydrogen production facility on the Norfolk coast. I said this.

Consider.

- Vattenfall’s Norfolk Zone is a 4.2 GW group of wind farms, which have all the requisite permissions and are shovel ready.

- Bacton Gas terminal has gas pipelines to Europe.

- Sizewell’s nuclear power stations will add security of supply.

- Extra wind farms could be added to the Norfolk Zone.

- Europe and especially Germany has a massive need for zero-carbon energy.

The only extra infrastructure needing to be built is the giant electrolyser.

I wouldn’t be surprised if RWE built a large electrolyser to supply Europe with hydrogen.

The big irony of this plan is that the BBL Pipeline between Bacton and the Netherlands was built, so that the UK could import Russian gas.

Could it in future be used to send the UK’s green hydrogen to Europe, so that some of that Russian gas can be replaced with a zero-carbon fuel?

Mathematical Modelling

There is a lot of graphs, maps and reasoning, which is used to detail how the authors obtained their conclusions.

Conclusion

This is the last paragraph of the paper.

Creating a hydrogen production industry is a transition story for UK’s oil and gas sector.

The UK is one of the few countries that could produce more hydrogen than it consumes in hydrocarbons today.

It is located in the centre of a vast resource, which premediates positioning itself at the centre of the European hydrogen supply chains.

Investing now to reduce costs and benefit from the generated value of exported hydrogen would make a reality out of the ambition to become the “Saudi Arabia of Wind”.

Boris may or may not have realised that what he said was possible.

But certainly make sure you read the paper from Imperial College.

RWE Acquires 4.2-Gigawatt UK Offshore Wind Development Portfolio From Vattenfall

The title of this post, is the same as that of this press release from RWE.

These three bullet points, act as sub-headings.

- Highly attractive portfolio of three projects at a late stage of development, with grid connections and permits secured, as well as advanced procurement of key components

- Delivery of the three Norfolk Offshore Wind Zone projects off the UK’s East Anglia coast will be part of RWE’s Growing Green investment and growth plans

- Agreed purchase price corresponds to an enterprise value of £963 million

These two paragraphs outline the deal.

RWE, one of the world’s leading offshore wind companies, will acquire the UK Norfolk Offshore Wind Zone portfolio from Vattenfall. The portfolio comprises three offshore wind development projects off the east coast of England – Norfolk Vanguard West, Norfolk Vanguard East and Norfolk Boreas.

The three projects, each with a planned capacity of 1.4 gigawatts (GW), are located 50 to 80 kilometres off the coast of Norfolk in East Anglia. This area is one of the world’s largest and most attractive areas for offshore wind. After 13 years of development, the three development projects have already secured seabed rights, grid connections, Development Consent Orders and all other key permits. The Norfolk Vanguard West and Norfolk Vanguard East projects are most advanced, having secured the procurement of most key components. The next milestone in the development of these two projects is to secure a Contract for Difference (CfD) in one of the upcoming auction rounds. RWE will resume the development of the Norfolk Boreas project, which was previously halted. All three Norfolk projects are expected to be commissioned in this decade.

There is also this handy map, which shows the location of the wind farms.

Note that there are a series of assets along the East Anglian coast, that will be useful to RWE’s Norfolk Zone development.

- In Vattenfall Selects Norfolk Offshore Wind Zone O&M Base, I talked about how the Port of Great Yarmouth will be the operational base for the Norfolk Zone wind farms.

- Bacton gas terminal has gas interconnectors to Belgium and the Netherlands lies between Cromer and Great Yarmouth.

- The cable to the Norfolk Zone wind farms is planned to make landfall between Bacton and Great Yarmouth.

- Sizewell is South of Lowestoft and has the 1.25 GW Sizewell B nuclear power station, with the 3.2 GW Sizewell C on its way, for more than adequate backup.

- Dotted around the Norfolk and Suffolk coast are 3.3 GW of earlier generations of wind farms, of which 1.2 GW have connections to RWE.

- The LionLink multipurpose 1.8 GW interconnector will make landfall to the North of Southwold

- There is also the East Anglian Array, which currently looks to be about 3.6 GW, that connects to the shore at Bawdsey to the South of Aldeburgh.

- For recreation, there’s Southwold.

- I can also see more wind farms squeezed in along the coast. For example, according to Wikipedia, the East Anglian Array could be increased in size to 7.2 GW.

It appears that a 15.5 GW hybrid wind/nuclear power station is being created on the North-Eastern coast of East Anglia.

The big problem is that East Anglia doesn’t really have any large use for electricity.

But the other large asset in the area is the sea.

- Undersea interconnectors can be built to other locations, like London or Europe, where there is a much greater need for electricity.

- In addition, the UK Government has backed a consortium, who have the idea of storing energy by using pressurised sea-water in 3D-printed concrete hemispheres under the sea. I wrote about this development in UK Cleantech Consortium Awarded Funding For Energy Storage Technology Integrated With Floating Wind.

A proportion of Russian gas in Europe, will have been replaced by Norfolk wind power and hydrogen, which will be given a high level of reliability from Suffolk nuclear power.

I have some other thoughts.

Would Hydrogen Be Easier To Distribute From Norfolk?

A GW-range electrolyser would be feasible but expensive and it would be a substantial piece of infrastructure.

I also feel, that placed next to Bacton or even offshore, there would not be too many objections from the Norfolk Nimbys.

Hydrogen could be distributed from the site in one of these ways.

- By road transport, as ICI did, when I worked in their hydrogen plant at Runcorn.

- I suspect, a rail link could be arranged, if there was a will.

- By tanker from the Port of Great Yarmouth.

- By existing gas interconnectors to Belgium and the Netherlands.

As a last resort it could be blended into the natural gas pipeline at Bacton.

In Major Boost For Hydrogen As UK Unlocks New Investment And Jobs, I talked about using the gas grid as an offtaker of last resort. Any spare hydrogen would be fed into the gas network, provided safety criteria weren’t breached.

I remember a tale from ICI, who from their refinery got a substantial amount of petrol, which was sold to independent petrol retailers around the North of England.

But sometimes they had a problem, in that the refinery produced a lot more 5-star petrol than 2-star. So sometimes if you bought 2-star, you were getting 5-star.

On occasions, it was rumoured that other legal hydrocarbons were disposed of in the petrol. I was once told that it was discussed that used diluent oil from polypropylene plants could be disposed of in this way. But in the end it wasn’t!

If hydrogen were to be used to distribute all or some of the energy, there would be less need for pylons to march across Norfolk.

Could A Rail Connection Be Built To The Bacton Gas Terminal

This Google Map shows the area between North Walsham and the coast.

Note.

- North Walsham is in the South-Western corner of the map.

- North Walsham station on the Bittern Line is indicated by the red icon.

- The Bacton gas terminal is the trapezoidal-shaped area on the coast, at the top of the map.

ThisOpenRailwayMap shows the current and former rail lines in the same area as the previous Google Map.

Note.

- North Walsham station is in the South-West corner of the map.

- The yellow track going through North Walsham station is the Bittern Line to Cromer and Sheringham.

- The Bacton gas terminal is on the coast in the North-East corner of the map.

I believe it would be possible to build a small rail terminal in the area with a short pipeline connection to Bacton, so that hydrogen could be distributed by train.

There used to be a branch line from North Walsham station to Cromer Beach station, that closed in 1953.

Until 1964 it was possible to get trains to Mundesley-on-Sea station.

So would it be possible to build a rail spur to the Bacton gas terminal along the old branch line?

In the Wikipedia entry for the Bittern Line this is said.

The line is also used by freight trains which are operated by GB Railfreight. Some trains carry gas condensate from a terminal at North Walsham to Harwich International Port.

The rail spur could have four main uses.

- Taking passengers to and from Mundesley-on-Sea and Bacton.

- Collecting gas condensate from the Bacton gas terminal.

- Collecting hydrogen from the Bacton gas terminal.

- Bringing in heavy equipment for the Bacton gas terminal.

It looks like another case of one of Dr. Beeching’s closures coming back to take a large chunk out of rail efficiency.

Claire Coutinho And Robert Habeck’s Tete-a-Tete

I wrote about their meeting in Downing Street in UK And Germany Boost Offshore Renewables Ties.

- Did Habeck run the RWE/Vattenfall deal past Coutinho to see it was acceptable to the UK Government?

- Did Coutinho lobby for SeAH to get the contract for the monopile foundations for the Norfolk Zone wind farms?

- Did Coutinho have a word for other British suppliers like iTMPower.

Note.

- I think we’d have heard and/or the deal wouldn’t have happened, if there had been any objections to it from the UK Government.

- In SeAH To Deliver Monopiles For Vattenfall’s 2.8 GW Norfolk Vanguard Offshore Wind Project, I detailed how SeAH have got the important first contract they needed.

So it appears so far so good.

Rackheath Station And Eco-Town

According to the Wikipedia entry for the Bittern Line, there are also plans for a new station at Rackheath to serve a new eco-town.

This is said.

A new station is proposed as part of the Rackheath eco-town. The building of the town may also mean a short freight spur being built to transport fuel to fire an on-site power station. The plans for the settlement received approval from the government in 2009.

The eco-town has a Wikipedia entry, which has a large map and a lot of useful information.

But the development does seem to have been ensnared in the planning process by the Norfolk Nimbys.

The Wikipedia entry for the Rackheath eco-town says this about the rail arrangements for the new development.

The current rail service does not allow room for an extra station to be added to the line, due to the length of single track along the line and the current signalling network. The current service at Salhouse is only hourly during peak hours and two-hourly during off-peak hours, as not all trains are able to stop due to these problems. Fitting additional trains to this very tight network would not be possible without disrupting the entire network, as the length of the service would increase, missing the connections to the mainline services. This would mean that a new 15-minute shuttle service between Norwich and Rackheath would have to be created; however, this would interrupt the main service and cause additional platforming problems. Finding extra trains to run this service and finding extra space on the platforms at Norwich railway station to house these extra trains poses additional problems, as during peak hours all platforms are currently used.

In addition, the plans to the site show that both the existing and the new rail station, which is being built 300m away from the existing station, will remain open.

. As the trains cannot stop at both stations, changing between the two services would be difficult and confusing, as this would involve changing stations.

I feel that this eco-town is unlikely to go ahead.

Did RWE Buy Vattenfall’s Norfolk Zone To Create Green Hydrogen For Europe?

Consider.

- Vattenfall’s Norfolk Zone is a 4.2 GW group of wind farms, which have all the requisite permissions and are shovel ready.

- Bacton Gas terminal has gas pipelines to Europe.

- Sizewell’s nuclear power stations will add security of supply.

- Extra wind farms could be added to the Norfolk Zone.

- Europe and especially Germany has a massive need for zero-carbon energy.

The only extra infrastructure needing to be built is the giant electrolyser.

I wouldn’t be surprised if RWE built a large electrolyser to supply Europe with hydrogen.