RWE And National Grid Answer New York Offshore Wind Call

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

Community Offshore Wind, a joint venture of RWE and National Grid Ventures, has submitted a proposal to the New York State Energy Research and Development Authority (NYSERDA) to develop 1.3 GW of new offshore wind capacity in response to New York’s expedited fourth competitive offshore wind solicitation.

These four paragraphs add more details.

This next phase of the project builds upon Community Offshore Wind’s provisional offtake award to deliver 1.3 GW of wind capacity as part of New York’s third solicitation for offshore wind. In total, the projects are expected to generate USD 4.4 billion in economic benefits to New York.

Combined with its provisionally awarded New York project, Community Offshore Wind is on track to deliver nearly USD 100 million in workforce and economic development investments, the developer said.

The new proposal includes nearly USD 50 million in funding for workforce and community initiatives, with a focus on creating opportunities for diverse New Yorkers and supporting local non-profit organizations.

The proposal also includes an investment of up to USD 10 million in the offshore wind supply chain, to help New York businesses prepare for the economic opportunities the growing industry will create. All of these commitments are contingent on NYSERDA’s final selections.

is this partly a result of the meeting between Energy Security Secretary Claire Coutinho and Germany’s Vice Chancellor, Robert Habeck, that I wrote abut in UK And Germany Boost Offshore Renewables Ties?

We certainly seem to be getting some good deals on renewable energy these days with the Germans and the Koreans.

Perhaps someone in the government is doing something right?

SeAH Wind Goes On Recruitment Spree For UK Monopile Factory

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

South Korea’s SeAH Wind has started its large-scale drive to recruit for positions including welders, platers, roll bending machine operatives, mechanical and electrical technicians, supervisors, and general operatives for its XXL monopile manufacturing facility on Teesworks, the UK.

These are the first two paragraphs.

Applications will be accepted via the company’s dedicated recruitment website where individuals can sign up for job alerts, register their expressions of interest, and apply directly for jobs.

SeAH Wind will hold events across multiple Teesside towns, including Middlesbrough, Redcar, Cleveland, and Hartlepool over the coming months where more details will be shared about vacancies and training opportunities at the South Bank site.

These three paragraphs talk about the education and training, and the number of jobs.

As part of the recruitment drive, the South Korean firm has also joined forces with Nordic Products and Services and Middlesbrough College to create two programmes under its SeAH Wind Academy programme.

During the 24-week training and development programme, 30 people will be trained to become welders for SeAH Wind.

Once fully operational, it is expected that a total of 750 direct jobs and 1,500 further supply chain jobs are set to come from the SeAH manufacturing facility.

I suspect, this the sort of investment that Teesside needs and will welcome.

Europe Installs Record-Breaking 4.2 GW Of Offshore Wind In 2023

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

Europe’s offshore wind industry brought online a record 4.2 GW of new capacity in 2023 and is expected to build around 5 GW of offshore wind annually over the next three years, according to WindEurope data. However, this is still not enough to meet the continent’s 2030 climate and energy security targets, WindEurope added.

These are the first two paragraphs.

The overall offshore wind capacity installed in 2023 was 40 per cent higher than in 2022. Of the 4.2 GW of new capacity, 3 GW was in the EU, an increase of 2.1 GW year on year, WindEurope said.

The Netherlands, France, and the UK installed the most new capacity, including the 1.5 GW Hollandse Kust Zuid offshore wind project in the Netherlands, according to the organisation.

But where are the Germans?

They’ve got plenty of steel and sea, Siemens make a lot of wind turbines and they certainly need the electricity.

In 2023, Germany generated their electricity as follows.

- Brown coal (17.7%)

- Hard coal (8.3%)

- Natural gas (10.5%)

- Wind (32.0%)

- Solar (12.2%)

- Biomass (9.7%)

- Nuclear (1.5%)

- Hydro (4.5%)

- Oil (0.7%)

- Other (2.9%)

By comparison the UK’s figures were.

- Coal (1%)

- Natural gas (32%)

- Wind (29.4%)

- Solar (4.9%)

- Biomass (5%)

- Nuclear (14.2%)

- Hydro (1.8%)

- Storage (1%)

- Imports (10.7%)

Note.

- The Germans use a lot of coal.

- The UK uses a lot more natural gas.

- Despite the much-criticised Drax, the Germans use twice as much biomass as we do.

- The UK uses tens times more nuclear.

The Wikipedia entries for German and UK wind power make interesting reading.

World’s First Floating Wind Farm To Undergo First Major Maintenance Campaign, Turbines To Be Towed To Norwegian Port

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

The world’s first commercial-scale floating wind farm, the 30 MW Hywind Scotland, officially entered the operations and maintenance (O&M) phase in October 2017. After a little over six years of operation, the wind farm’s Siemens Gamesa wind turbines are now due for some major maintenance work.

And this is the first paragraph.

While offshore wind farms undergo turbine maintenance work more than once during their lifespans and tasks such as major component exchange are nothing uncommon, this is the first time a campaign of this kind will be done on a floating farm.

Hywind Scotland has a web site, where this is said on the home page.

The world’s first floating wind farm, the 30 MW Hywind Scotland pilot park, has been in operation since 2017, demonstrating the feasibility of floating wind farms that could be ten times larger.

Equinor and partner Masdar invested NOK 2 billion to realise Hywind Scotland, achieving a 60-70% cost reduction compared with the Hywind Demo project in Norway. Hywind Scotland started producing electricity in October 2017.

Each year since Hywind Scotland started production the floating wind farm has achieved the highest average capacity factor of all UK offshore windfarms, proving the potential of floating offshore wind farms.

This news item from Equinor is entitled Equinor Marks 5 Years Of Operations At World’s First Floating Wind Farm, says this about the capacity factor of Hywind Scotland.

Hywind Scotland, located off the coast of Peterhead, Scotland, is the world’s first floating offshore wind farm and the world’s best-performing offshore wind farm, achieving a capacity factor of 54% over its five years of operations. Importantly, Hywind Scotland has run to high safety standards, marking five years of no loss time injuries during its operation.

Any capacity factor over 50 % is excellent and is to be welcomed.

Maintaining A Floating Wind Farm

One of the supposed advantages of floating wind farms, is that the turbines can be towed into port for maintenance.

This first major maintenance of a floating wind farm, will test that theory and hopefully provide some spectacular pictures.

UK Offshore Wind In 2030

With the election coming up in the next year, I thought I’d add how much offshore wind will be available in the next few years.

In October 2023, according to this Wikipedia entry, there were offshore wind farms consisting of 2,695 turbines with a combined capacity of 14,703 megawatts.

These wind farms are due to be commissioned between now and the end of 2030.

- Dogger Bank A – 1235 MW – 2023

- Neart Na Gaoithe – 450 MW – 2024

- Dogger Bank B – 1235 MW – 2024

- Forthwind – 12 MW – 2024

- Moray West – 882 MW – 2025

- Dogger Bank C – 1218 MW – 2025

- Sofia Offshore Wind Farm – 1400 MW – 2026

- East Anglia 3 – 1372 MW – 2026

- East Anglia One North – 800 MW – 2026

- East Anglia Two – 900 MW – 2026

- Pentland – 100 MW – 2026 – Floating

- Hornsea Three – 2852 MW – 2027

- Norfolk Boreas, Phase 1 – 1380 MW – 2027

- Llŷr 1 – 100 MW – 2027 – Floating

- Llŷr 2 – 100 MW – 2027 – Floating

- Whitecross – 100 MW – 2027 – Floating

- Morecambe – 480 MW – 2028

- Bellrock – 1200 MW – 2028 – Floating

- Mona – 1500 MW – 2029

- Morgan – 1500 MW – 2029

- West of Orkney – 2000 MW – 2029

- Rampion 2 Extension – 1200 MW – 2030

- Norfolk Vanguard East – 1380 MW – 2030

- Morven – 2907 MW – 2030

- Norfolk Vanguard West – 1380 MW – 2030

- Berwick Bank – 4100 MW – 2030

- Outer Dowsing – 1500 MW – 2030

- Broadshore – 900 MW – 2028 – Floating

- Caledonia – 2000 MW – 2030

- Stromar – 1000 MW – 2028 – Floating

- N3 Project – 495 MW – 2030

- Muir Mhòr – 798 MW – 2030 – Floating

- North Falls – 504 MW – 2030

- Spiorad na Mara – 840 MW – 2031

- Bowdun – 1008 MW – 2033

- Ayre – 1008 MW – 2033 – Floating

- Buchan – 960 MW – 2033 – Floating

These can give these totals for the next few years.

- 2023 – 14.70 GW

- 2024 – 17.64 GW

- 2025 19.74 GW

- 2026 – 24.31 GW

- 2027 – 28.81 GW

- 2028 – 32.39 GW

- 2029 – 37.39 GW

- 2030 – 53.65 GW

- 2031 – 54.50 GW

- 2032 – 54.50 GW

- 2033 – 57.47 GW

Note.

- The Government’s 50 GW target of offshore wind power by 2030 has been achieved.

- A total of 7.27 GW of floating wind power has been installed.

- The Government’s target of 5 GW of floating offshore wind power by 2030 has also been achieved.

Currently, the UK is generating 37.49 GW of electricity.

Japanese Offshore Wind And Battery Storage Project Begins Commercial Operation

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

On 1 January 2024, JERA and Green Power Investment Corporation (GPI) began commercial operations at the 112 MW Ishikari Bay New Port Offshore Wind Farm in Japan, which they own through Green Power Ishikari GK, a special-purpose corporation (SPC).

The most significant thing about this wind farm, is that it has been designed from Day One to operate with a battery, which is detailed in the last paragraph.

The project also features a battery storage component with 100 MW x 180 MWh of capacity.

Note that the output of the battery is 89 % of that of the wind farm. Is that the ideal ratio between battery and wind farm capacities?

Conclusion

Because of my training, as an Electronics and Control Engineer, I belief that most renewable energy can be smoothed with the adding of a battery.

Offshore Wind Turbines In 2023: 16 MW Model Installed Offshore, 18 MW WTGs Selected For New Project, 22 MW Turbine Announced

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

The biggest wind turbines also make for some of the biggest news on offshoreWIND.biz. In 2023, wind turbine OEMs continued making headlines with their models in development and on the path to commercialisation, and by announcing brand new wind turbine generators (WTGs) that further raise the bar in generation capacity and size. Here, we are bringing an overview of the biggest and most powerful wind turbines we reported about in 2023.

This is the first paragraph.

Some of the wind turbines from our lookback article from a year ago, which were announced or launched in 2022, have now advanced to being installed offshore and/or are already being selected for commercial offshore wind projects that are planned to be built in the not-so-distant future.

Offshore wind turbines are certainly getting larger.

- The Chinese seem to be leading the way with turbines that produce over 20 MW, but European and US manufacturers appear to be looking at 16-18 MW.

- This compares with typical farms commissioned in the last few years of about 13-14 MW, which is roughly a 26 % increase in size.

- In Crown Estate Mulls Adding 4 GW Of Capacity From Existing Offshore Wind Projects, I talk about how bigger turbine sizes could be increased in wind farms, that are being planned.

I feel the UK, could benefit from this increase in wind turbine size.

BP And EnBW To Run Suction Bucket Trials At UK Offshore Wind Farm Sites

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

On 30 December, the vessel North Sea Giant is expected to start suction bucket trials within the array areas of the Mona and Morgan offshore wind farm sites, located off North West England and North Wales.

These are the first three paragraphs.

The trials will run for an estimated 32 days, during which time the vessel will be lifting a suction bucket and setting it down on the seabed, and using subsea pumps to drive the suction bucket into the seabed and back out.

The campaign is expected to consist of around 20 suction bucket trials, subject to weather conditions.

In their environmental impact assessment (EIA) scoping reports, issued last year, BP and EnBW state that a number of foundation types are being considered for the two proposed offshore wind farms and that the type(s) to be used will not be confirmed until the final design, after the projects are granted consent.

It sounds sensible to try out different types of foundations, but what is a suction bucket?

This page on the Ørsted web site is entitled Our Experience With Suction Bucket Jackets, explains how they work and are installed.

This is the first paragraph.

Monopiles (MPs) are currently the most commonly used foundation solution for offshore wind turbines with 81% of offshore wind turbines in European waters founded on MPs at the end of 2019 (Wind Europe, 2020). Where site conditions do not allow for an efficient or practical MP design, a number of alternative foundation solutions are available, including the suction bucket jacket (SBJ), piled jacket, gravity base or even a floating solution.

These two paragraphs, indicate when Ørsted has used SBJs.

Ørsted installed the world’s first SBJ for an offshore WTG at the Borkum Riffgrund 1 offshore windfarm in Germany in 2014.

Since the installation of the Borkum Riffgrund 1 SBJ, Ørsted has been involved in the design and installation of SBJs at the Borkum Riffgrund 2 and the design for Hornsea 1 offshore wind farms. At Hornsea 1, overall project timeline considerations and limitations of serial production capacities precluded the use of SBJs, and therefore the project chose an alternative foundation type.

It will be interesting to see how BP and EnBW’s trial gets on.

Enabling The UK To Become The Saudi Arabia Of Wind?

The title of this post, is the same as that of a paper from Imperial College.

The paper can be downloaded from this page of the Imperial College web site.

This is a paragraph from the Introduction of the paper.

In December 2020, the then Prime Minister outlined the government’s ten-point plan for a green industrial revolution, expressing an ambition “to turn the UK into the Saudi Arabia of wind power generation, enough wind power by 2030 to supply every single one of our homes with electricity”.

The reference to Saudi Arabia, one of the world’s largest oil producers for many decades, hints at the significant role the UK’s energy ambitions hoped to play in the global economy.

Boris Johnson was the UK Prime Minister at the time, so was his statement just his usual bluster or a simple deduction from the facts.

The paper I have indicated is a must-read and I do wonder if one of Boris’s advisors had read the paper before Boris’s speech. But as the paper appears to have been published in September 2023, that is not a valid scenario.

The paper though is full of important information.

The Intermittency Of Wind And Solar Power

The paper says this about the intermittency of wind and solar power.

One of the main issues is the intermittency of solar and wind electricity generation, which means it cannot be relied upon without some form of backup or sufficient storage.

Solar PV production varies strongly along both the day-night and seasonal cycles. While output is higher during the daytime (when demand is

higher than overnight), it is close to zero when it is needed most, during the times of peak electricity demand (winter evenings from 5-6 PM).At present, when wind output is low, the UK can fall back to fossil fuels to make up for the shortfall in electricity supply. Homes stay warm, and cars keep moving.

If all sectors were to run on variable renewables, either the country needs to curb energy usage during shortfalls (unlikely to be popular with consumers), accept continued use of fossil fuels across all sectors (incompatible with climate targets), or develop a large source of flexibility such as energy storage (likely to be prohibitively expensive at present).

The intermittency of wind and solar power means we have a difficult choice to make.

The Demand In Winter

The paper says this about the demand in winter.

There are issues around the high peaks in heating demand during winter, with all-electric heating very expensive to serve (as

the generators built to serve that load are only

needed for a few days a year).Converting all the UK’s vehicles to EVs would increase total electricity demand from 279 TWh to 395 TWh. Switching all homes across the country to heat pumps would increase demand by a further 30% to 506 TWh.

This implies that the full electrification of the heating and transport sectors would increase the annual power needs in the country by 81%.

This will require the expansion of the electricity system (transmission capacity, distribution grids, transformers,

substations, etc.), which would pose serious social, economic and technical challenges.Various paths, policies and technologies for the decarbonisation of heating, transport, and industrial emissions must be considered in order for the UK to meet its zero-emission targets.

It appears that electrification alone will not keep us warm, power our transport and keep our industry operating.

The Role Of Hydrogen

The paper says this about the role of hydrogen.

Electrifying all forms of transport might prove difficult (e.g., long-distance heavy goods) or nigh impossible (e.g., aviation) due to the high energy density requirements, which current batteries cannot meet.

Hydrogen has therefore been widely suggested as a low-carbon energy source for these sectors, benefiting from high energy density (by weight), ease of storage (relative to electricity) and its versatility to be used in many ways.

Hydrogen is also one of the few technologies capable of

providing very long-duration energy storage (e.g., moving energy between seasons), which is critical to supporting the decarbonisation of the whole energy system with high shares of renewables because it allows times of supply and demand mismatch to be managed over both short and long timescales.It is a clean alternative to fossil fuels as its use (e.g., combustion) does not emit any CO2.

Hydrogen appears to be ideal for difficult to decarbonise sectors and for storing energy for long durations.

The Problems With Hydrogen

The paper says this about the problems with hydrogen.

The growth of green hydrogen technology has been held back by the high cost, lack of existing infrastructure, and its lower efficiency

of conversion.Providing services with hydrogen requires two to three times more primary energy than direct use of electricity.

There is a lot of development to be done before hydrogen is as convenient and affordable as electricity and natural gas.

Offshore Wind

The paper says this about offshore wind.

Offshore wind is one of the fastest-growing forms of renewable energy, with the UK taking a strong lead on the global stage.

Deploying wind turbines offshore typically leads to a higher electricity output per turbine, as there are typically higher wind speeds and fewer obstacles to obstruct wind flow (such as trees and buildings).

The productivity of the UK’s offshore wind farms is nearly 50% higher than that of onshore wind farms.

Offshore wind generation also typically has higher social acceptability as it avoids land usage conflicts and has a lower visual impact.

To get the most out of this resource, very large structures (more than twice the height of Big Ben) must be connected to the ocean floor and operate in the harshest conditions for decades.

Offshore wind turbines are taller and have larger rotor diameters than onshore wind turbines, which produces a more consistent and higher output.

Offshore wind would appear to be more efficient and better value than onshore.

The Scale Of Offshore Wind

The paper says this about the scale of offshore wind.

The geographical distribution of offshore wind is heavily skewed towards Europe, which hosts over 80% of the total global offshore wind capacity.

This can be attributed to the good wind conditions and the shallow water depths of the North Sea.

The UK is ideally located to take advantage of offshore wind due to its extensive resource.

The UK could produce over 6000 TWh of electricity if the offshore wind resources in all the feasible area of the exclusive economic zone (EEZ) is exploited.

Note.

- 6000 TWh of electricity per annum would need 2740 GW of wind farms if the average capacity factor was a typical 25 %.

- At a price of 37.35 £/MWh, 6000 TWh would be worth $224.1 billion.

Typically, most domestic users seem to pay about 30 pence per KWh.

The Cost Of Offshore Wind

The paper says this about the cost of offshore wind.

The cost of UK offshore wind has fallen because of the reductions in capital expenditure (CapEx), operational expenditure (OpEx), and financing costs.

This has been supported by the global roll-out of bigger offshore wind turbines, hence, causing an increase in offshore wind energy capacity.

This increase in installed capacity has been fuelled by several low-carbon support schemes from the UK government.

The effect of these schemes can be seen in the UK 2017 Contracts for Difference (CfD) auctions where offshore wind reached strike prices as low as 57.50 £/MWh and an even lower strike price of 37.35 £/MWh in 2022.

Costs and prices appear to be going the right way.

The UK’s Offshore Wind Targets

The paper says this about the UK’s offshore wind targets.

The offshore wind capacity in the UK has grown over the past decade.

Currently, the UK has a total offshore wind capacity of 13.8GW, which is sufficient to power more than 10 million homes.

This represents a more than fourfold increase compared to the capacity installed in 2012.

The UK government has set ambitious targets for offshore wind development.

In 2019, the target was to install a total of 40 GW of offshore wind capacity by 2030, and this was later raised to 50 GW, with up to 5 GW of floating offshore wind.

This will play a pivotal role in decarbonising the UK’s power system by the government’s deadline of 2035.

As I write this, the UK’s total electricity production is 31.8 GW. So 50 GW of wind will go a good way to providing the UK with zero-carbon energy. But it will need a certain amount of reliable alternative power sources for when the wind isn’t blowing.

The UK’s Hydrogen Targets

The paper says this about the UK’s hydrogen targets.

The UK has a target of 10 GW of low-carbon hydrogen production to be deployed by 2030, as set out in the British Energy Security Strategy.

Within this target, there is an ambition for at least half of the 10 GW of production capacity to be met through green hydrogen production technologies (as opposed to hydrogen produced from steam methane reforming using carbon capture).

Modelling conducted by the Committee on Climate Change in its Sixth Carbon Budget estimated that demand for low-carbon hydrogen across the whole country could reach 161–376 TWh annually by 2050, comparable in scale to the total electricity demand.

We’re going to need a lot of electrolyser capacity.

Pairing Hydrogen And Offshore Wind

The paper says this about pairing hydrogen and offshore wind.

Green hydrogen holds strong potential in addressing the intermittent nature of renewable generation sources, particularly wind and solar energy, which naturally fluctuate due to weather conditions.

Offshore wind in particular is viewed as being a complementary technology to pair with green hydrogen production, due to three main factors: a) the high wind energy capacity factors offshore, b) the potential for large-scale deployment and c) hydrogen as a supporting technology for offshore wind energy integration.

It looks like a match made in the waters around the UK.

The Cost Of Green Hydrogen

The paper says this about the cost of green hydrogen.

The cost of green hydrogen is strongly influenced by the price of the electrolyser unit itself.

If the electrolyser is run more intensively over the course of the lifetime of the plant, a larger volume of hydrogen will be produced and so the cost of the electrolyser will be spread out more, decreasing the cost per unit of produced hydrogen.

If the variable renewable electricity source powering the electrolyser has a higher capacity factor, this will contribute towards a

lower cost of hydrogen produced.Offshore wind in the UK typically has a higher capacity factor than onshore wind energy (up to 20%), and is around five times higher than solar, so pairing

offshore wind with green hydrogen production is of interest.

It would appear that any improvements in wind turbine and electrolyser efficiency would be welcomed.

The Size Of Wind Farms

The paper says this about the size of wind farms.

Offshore wind farms can also be larger scale, due to increased availability of space and reduced restrictions on tip heights due to planning permissions.

The average offshore wind turbine in the UK had a capacity of 3.6 MW in 2022, compared to just 2.5-3 MW for onshore turbines.

As there are fewer competing uses for space, offshore wind can not only have larger turbines but the wind farms can comprise many more turbines.

Due to the specialist infrastructure requirements for hydrogen transport and storage, and the need for economies of scale to reduce the costs of

production, pairing large-scale offshore wind electricity generation with green hydrogen

production could hold significant benefits.

I am not surprised that economies of scale give benefits.

The Versatility Of Hydrogen

The paper says this about the versatility of hydrogen.

Hydrogen is a highly adaptable energy carrier with numerous potential applications and has been anticipated by some as playing a key role in the future energy system, especially when produced through electrolysis.

It could support the full decarbonisation of “hard to decarbonise” processes within the UK industrial sector, offering a solution for areas which may be difficult to electrify or are heavily reliant on fossil fuels for high-temperature heat.

When produced through electrolysis, it could be paired effectively as an energy storage technology with offshore wind, with the potential to store energy across seasons with little to no energy degradation and transport low-carbon energy internationally.

The UK – with its significant offshore wind energy resources and targets – could play a potentially leading role in producing green hydrogen to both help its pathway to net zero, and potentially create a valuable export industry.

In RWE Acquires 4.2-Gigawatt UK Offshore Wind Development Portfolio From Vattenfall, I postulated that RWE may have purchased Vattenfall’s 4.2 GW Norfolk Zone of windfarms to create a giant hydrogen production facility on the Norfolk coast. I said this.

Consider.

- Vattenfall’s Norfolk Zone is a 4.2 GW group of wind farms, which have all the requisite permissions and are shovel ready.

- Bacton Gas terminal has gas pipelines to Europe.

- Sizewell’s nuclear power stations will add security of supply.

- Extra wind farms could be added to the Norfolk Zone.

- Europe and especially Germany has a massive need for zero-carbon energy.

The only extra infrastructure needing to be built is the giant electrolyser.

I wouldn’t be surprised if RWE built a large electrolyser to supply Europe with hydrogen.

The big irony of this plan is that the BBL Pipeline between Bacton and the Netherlands was built, so that the UK could import Russian gas.

Could it in future be used to send the UK’s green hydrogen to Europe, so that some of that Russian gas can be replaced with a zero-carbon fuel?

Mathematical Modelling

There is a lot of graphs, maps and reasoning, which is used to detail how the authors obtained their conclusions.

Conclusion

This is the last paragraph of the paper.

Creating a hydrogen production industry is a transition story for UK’s oil and gas sector.

The UK is one of the few countries that could produce more hydrogen than it consumes in hydrocarbons today.

It is located in the centre of a vast resource, which premediates positioning itself at the centre of the European hydrogen supply chains.

Investing now to reduce costs and benefit from the generated value of exported hydrogen would make a reality out of the ambition to become the “Saudi Arabia of Wind”.

Boris may or may not have realised that what he said was possible.

But certainly make sure you read the paper from Imperial College.

RWE Acquires 4.2-Gigawatt UK Offshore Wind Development Portfolio From Vattenfall

The title of this post, is the same as that of this press release from RWE.

These three bullet points, act as sub-headings.

- Highly attractive portfolio of three projects at a late stage of development, with grid connections and permits secured, as well as advanced procurement of key components

- Delivery of the three Norfolk Offshore Wind Zone projects off the UK’s East Anglia coast will be part of RWE’s Growing Green investment and growth plans

- Agreed purchase price corresponds to an enterprise value of £963 million

These two paragraphs outline the deal.

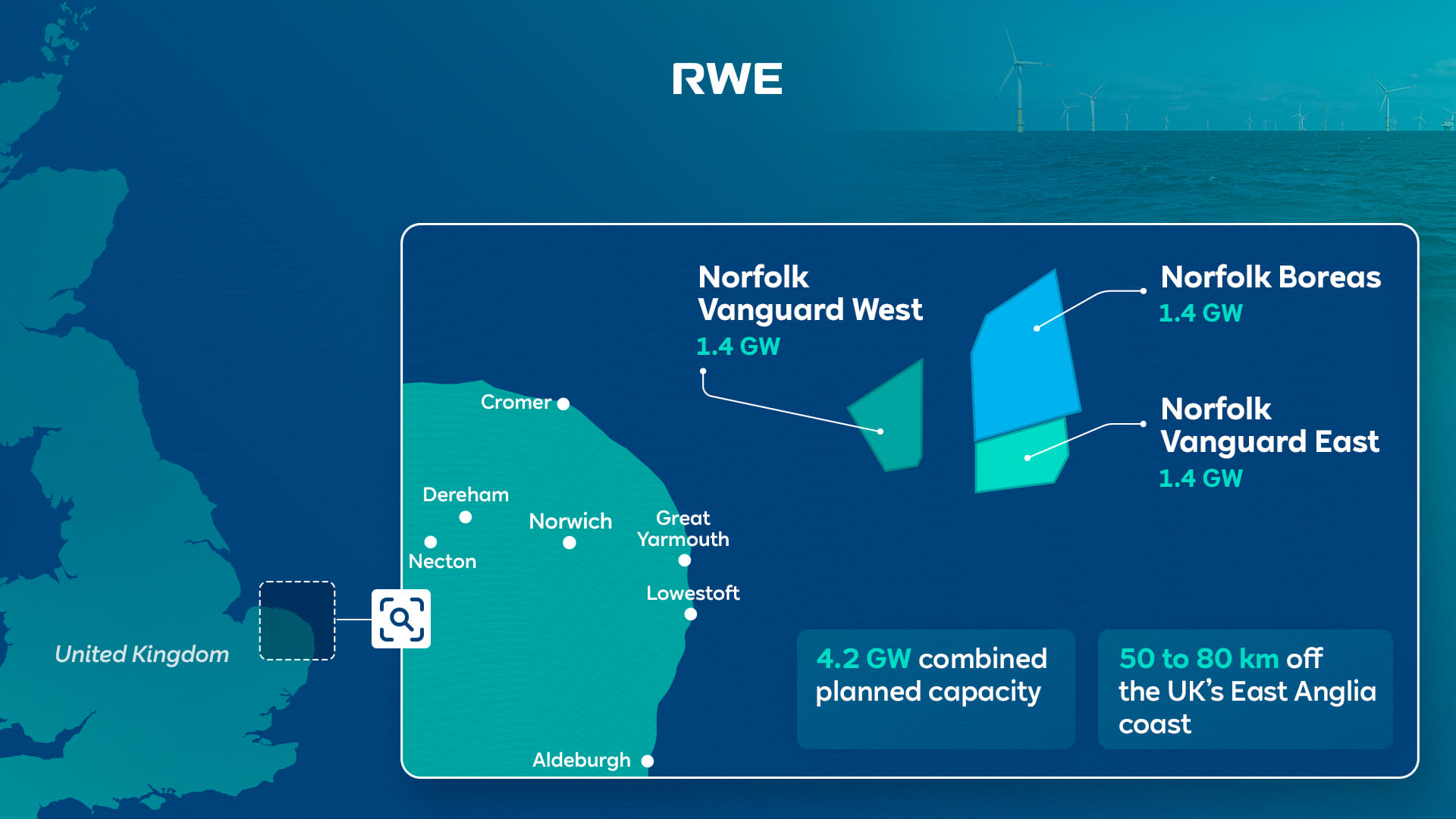

RWE, one of the world’s leading offshore wind companies, will acquire the UK Norfolk Offshore Wind Zone portfolio from Vattenfall. The portfolio comprises three offshore wind development projects off the east coast of England – Norfolk Vanguard West, Norfolk Vanguard East and Norfolk Boreas.

The three projects, each with a planned capacity of 1.4 gigawatts (GW), are located 50 to 80 kilometres off the coast of Norfolk in East Anglia. This area is one of the world’s largest and most attractive areas for offshore wind. After 13 years of development, the three development projects have already secured seabed rights, grid connections, Development Consent Orders and all other key permits. The Norfolk Vanguard West and Norfolk Vanguard East projects are most advanced, having secured the procurement of most key components. The next milestone in the development of these two projects is to secure a Contract for Difference (CfD) in one of the upcoming auction rounds. RWE will resume the development of the Norfolk Boreas project, which was previously halted. All three Norfolk projects are expected to be commissioned in this decade.

There is also this handy map, which shows the location of the wind farms.

Note that there are a series of assets along the East Anglian coast, that will be useful to RWE’s Norfolk Zone development.

- In Vattenfall Selects Norfolk Offshore Wind Zone O&M Base, I talked about how the Port of Great Yarmouth will be the operational base for the Norfolk Zone wind farms.

- Bacton gas terminal has gas interconnectors to Belgium and the Netherlands lies between Cromer and Great Yarmouth.

- The cable to the Norfolk Zone wind farms is planned to make landfall between Bacton and Great Yarmouth.

- Sizewell is South of Lowestoft and has the 1.25 GW Sizewell B nuclear power station, with the 3.2 GW Sizewell C on its way, for more than adequate backup.

- Dotted around the Norfolk and Suffolk coast are 3.3 GW of earlier generations of wind farms, of which 1.2 GW have connections to RWE.

- The LionLink multipurpose 1.8 GW interconnector will make landfall to the North of Southwold

- There is also the East Anglian Array, which currently looks to be about 3.6 GW, that connects to the shore at Bawdsey to the South of Aldeburgh.

- For recreation, there’s Southwold.

- I can also see more wind farms squeezed in along the coast. For example, according to Wikipedia, the East Anglian Array could be increased in size to 7.2 GW.

It appears that a 15.5 GW hybrid wind/nuclear power station is being created on the North-Eastern coast of East Anglia.

The big problem is that East Anglia doesn’t really have any large use for electricity.

But the other large asset in the area is the sea.

- Undersea interconnectors can be built to other locations, like London or Europe, where there is a much greater need for electricity.

- In addition, the UK Government has backed a consortium, who have the idea of storing energy by using pressurised sea-water in 3D-printed concrete hemispheres under the sea. I wrote about this development in UK Cleantech Consortium Awarded Funding For Energy Storage Technology Integrated With Floating Wind.

A proportion of Russian gas in Europe, will have been replaced by Norfolk wind power and hydrogen, which will be given a high level of reliability from Suffolk nuclear power.

I have some other thoughts.

Would Hydrogen Be Easier To Distribute From Norfolk?

A GW-range electrolyser would be feasible but expensive and it would be a substantial piece of infrastructure.

I also feel, that placed next to Bacton or even offshore, there would not be too many objections from the Norfolk Nimbys.

Hydrogen could be distributed from the site in one of these ways.

- By road transport, as ICI did, when I worked in their hydrogen plant at Runcorn.

- I suspect, a rail link could be arranged, if there was a will.

- By tanker from the Port of Great Yarmouth.

- By existing gas interconnectors to Belgium and the Netherlands.

As a last resort it could be blended into the natural gas pipeline at Bacton.

In Major Boost For Hydrogen As UK Unlocks New Investment And Jobs, I talked about using the gas grid as an offtaker of last resort. Any spare hydrogen would be fed into the gas network, provided safety criteria weren’t breached.

I remember a tale from ICI, who from their refinery got a substantial amount of petrol, which was sold to independent petrol retailers around the North of England.

But sometimes they had a problem, in that the refinery produced a lot more 5-star petrol than 2-star. So sometimes if you bought 2-star, you were getting 5-star.

On occasions, it was rumoured that other legal hydrocarbons were disposed of in the petrol. I was once told that it was discussed that used diluent oil from polypropylene plants could be disposed of in this way. But in the end it wasn’t!

If hydrogen were to be used to distribute all or some of the energy, there would be less need for pylons to march across Norfolk.

Could A Rail Connection Be Built To The Bacton Gas Terminal

This Google Map shows the area between North Walsham and the coast.

Note.

- North Walsham is in the South-Western corner of the map.

- North Walsham station on the Bittern Line is indicated by the red icon.

- The Bacton gas terminal is the trapezoidal-shaped area on the coast, at the top of the map.

ThisOpenRailwayMap shows the current and former rail lines in the same area as the previous Google Map.

Note.

- North Walsham station is in the South-West corner of the map.

- The yellow track going through North Walsham station is the Bittern Line to Cromer and Sheringham.

- The Bacton gas terminal is on the coast in the North-East corner of the map.

I believe it would be possible to build a small rail terminal in the area with a short pipeline connection to Bacton, so that hydrogen could be distributed by train.

There used to be a branch line from North Walsham station to Cromer Beach station, that closed in 1953.

Until 1964 it was possible to get trains to Mundesley-on-Sea station.

So would it be possible to build a rail spur to the Bacton gas terminal along the old branch line?

In the Wikipedia entry for the Bittern Line this is said.

The line is also used by freight trains which are operated by GB Railfreight. Some trains carry gas condensate from a terminal at North Walsham to Harwich International Port.

The rail spur could have four main uses.

- Taking passengers to and from Mundesley-on-Sea and Bacton.

- Collecting gas condensate from the Bacton gas terminal.

- Collecting hydrogen from the Bacton gas terminal.

- Bringing in heavy equipment for the Bacton gas terminal.

It looks like another case of one of Dr. Beeching’s closures coming back to take a large chunk out of rail efficiency.

Claire Coutinho And Robert Habeck’s Tete-a-Tete

I wrote about their meeting in Downing Street in UK And Germany Boost Offshore Renewables Ties.

- Did Habeck run the RWE/Vattenfall deal past Coutinho to see it was acceptable to the UK Government?

- Did Coutinho lobby for SeAH to get the contract for the monopile foundations for the Norfolk Zone wind farms?

- Did Coutinho have a word for other British suppliers like iTMPower.

Note.

- I think we’d have heard and/or the deal wouldn’t have happened, if there had been any objections to it from the UK Government.

- In SeAH To Deliver Monopiles For Vattenfall’s 2.8 GW Norfolk Vanguard Offshore Wind Project, I detailed how SeAH have got the important first contract they needed.

So it appears so far so good.

Rackheath Station And Eco-Town

According to the Wikipedia entry for the Bittern Line, there are also plans for a new station at Rackheath to serve a new eco-town.

This is said.

A new station is proposed as part of the Rackheath eco-town. The building of the town may also mean a short freight spur being built to transport fuel to fire an on-site power station. The plans for the settlement received approval from the government in 2009.

The eco-town has a Wikipedia entry, which has a large map and a lot of useful information.

But the development does seem to have been ensnared in the planning process by the Norfolk Nimbys.

The Wikipedia entry for the Rackheath eco-town says this about the rail arrangements for the new development.

The current rail service does not allow room for an extra station to be added to the line, due to the length of single track along the line and the current signalling network. The current service at Salhouse is only hourly during peak hours and two-hourly during off-peak hours, as not all trains are able to stop due to these problems. Fitting additional trains to this very tight network would not be possible without disrupting the entire network, as the length of the service would increase, missing the connections to the mainline services. This would mean that a new 15-minute shuttle service between Norwich and Rackheath would have to be created; however, this would interrupt the main service and cause additional platforming problems. Finding extra trains to run this service and finding extra space on the platforms at Norwich railway station to house these extra trains poses additional problems, as during peak hours all platforms are currently used.

In addition, the plans to the site show that both the existing and the new rail station, which is being built 300m away from the existing station, will remain open.

. As the trains cannot stop at both stations, changing between the two services would be difficult and confusing, as this would involve changing stations.

I feel that this eco-town is unlikely to go ahead.

Did RWE Buy Vattenfall’s Norfolk Zone To Create Green Hydrogen For Europe?

Consider.

- Vattenfall’s Norfolk Zone is a 4.2 GW group of wind farms, which have all the requisite permissions and are shovel ready.

- Bacton Gas terminal has gas pipelines to Europe.

- Sizewell’s nuclear power stations will add security of supply.

- Extra wind farms could be added to the Norfolk Zone.

- Europe and especially Germany has a massive need for zero-carbon energy.

The only extra infrastructure needing to be built is the giant electrolyser.

I wouldn’t be surprised if RWE built a large electrolyser to supply Europe with hydrogen.