How Germany Is Dominating Hydrogen Market

The title of this post, is the same as that of this article on Hydrogen Fuel News.

This is the sub heading.

With 3827 kilometers of pipeline across the country, Germany is blazing a trail through the continent in terms of hydrogen infrastructure growth.

These are the first two paragraphs.

Indeed, plans within the country are so far advanced that Germany is set to become the biggest importer of hydrogen in Europe and the third biggest in the world, behind global leaders China and Japan.

All this leaves the German transport sector in good stead, with a strong infrastructure supporting clean fuel adoption, while the country transitions towards net zero.

So where are the Germans going to get their hydrogen from?

One possibility is the UK.

- The UK has vast amounts of renewable energy.

- We’re only hundreds of kilometres, instead of thousands of kilometres away.

- RWE; the German energy giant has full or partial interests in about 12,3 GW of UK wind farms.

- RWE is building the Pembroke Net Zero Centre which will generate green and blue hydrogen.

Hydrogen could be exported from the UK to Germany by tanker.

Conclusion

Production and exporting of green hydrogen will become significant industry in the UK.

Ørsted Secures Exclusive Access To Lower-Emission Steel From Dillinger

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

Ørsted will be offered the first production of lower-emission steel from German-based Dillinger, subject to availability and commercial terms and conditions. The steel plates are intended to be used for offshore wind monopile foundations in future projects.

These three paragraphs outline the deal.

Under a large-scale supply agreement entered into in 2022, Ørsted will procure significant volumes of regular heavy plate steel from 2024, giving the company access at scale to and visibility of the most crucial raw material in offshore wind while supporting Dillinger to accelerate investments in new lower-emission steel production, according to Ørsted.

The Danish renewable energy giant expects to be able to procure lower-emission steel produced at Dillinger’s facility in Dillingen, Germany, from 2027-2028.

Taking the current technology outlook into account, the reduction of the process-related carbon emissions from production is expected to be around 55-60 per cent compared to conventional heavy plate steel production, Ørsted said.

Increasingly, we’ll see lower emission steel and concrete used for wind turbine foundations.

This press release on the Dillinger web site is entitled Historic Investment For Greater Climate Protection: Supervisory Boards Approve Investment Of EUR 3.5 billion For Green Steel From Saarland.

These are two paragraphs from the press release.

Over the next few years leading up to 2027, in addition to the established blast furnace route, the new production line with an electric arc furnace (EAF) will be built at the Völklingen site and an EAF and direct reduced iron (DRI) plant for the production of sponge iron will be built at the Dillinger plant site. Transformation branding has also been developed to visually represent the transformation: “Pure Steel+”. The message of “Pure Steel+” is that Saarland’s steel industry will retain its long-established global product quality, ability to innovate, and culture, even in the transformation. The “+” refers to the carbon-neutrality of the products.

The availability of green hydrogen at competitive prices is a basic precondition for this ambitious project to succeed, along with prompt funding commitments from Berlin and Brussels. Local production of hydrogen will therefore be established as a first step together with the local energy suppliers, before connecting to the European hydrogen network to enable use of hydrogen to be increased to approx. 80 percent. The Saarland steel industry is thus laying the foundation for a new hydrogen-based value chain in the Saarland, in addition to decarbonizing its own production. In this way, SHS – Stahl-Holding-Saar is supporting Saarland on its path to becoming a model region for transformation.

It sounds to me, that Tata Steel could be doing something similar at Port Talbot.

- Tata want to build an electric arc furnace to replace the blast furnaces.

- There will be plenty of green electricity from the Celtic Sea.

- RWE are planning a very large hydrogen electrolyser in Pembroke.

- Celtic Sea offshore wind developments would probably like a supply of lower emission steel on their door-step.

I would suspect, that Welsh steel produced by an electric arc furnace will match the quality of the German steel, that is made the same way.

Work Starts On World’s Largest Floating Solar Project, Part of RWE’s OranjeWind

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

The Nautical SUNRISE consortium partners have commenced the project whose goal is to facilitate research and development of offshore floating solar systems and its components. The project aims to integrate a 5 MW offshore floating solar system within RWE’s OranjeWind, a wind farm to be built 53 kilometres off the Dutch coast.

These three paragraphs outline the project.

Research and development on the offshore floating solar (OFS) systems and its components of the EUR 8.4 million project, supported by EUR 6.8 million of the Horizon Europe programme, kicked off in December 2023.

The project will enable the large-scale deployment and commercialisation of offshore floating solar systems in the future, both as standalone systems and integrated into offshore wind farms.

The project aims to design, build, and showcase a 5 MW OFS system using the modular solution of the Dutch floating company SolarDuck.

Note.

- It’s only the fourth of March and this is the second floating solar project of the month.

- The first was SolarDuck, Green Arrow Capital And New Developments S.R.L. Sign Collaboration Agreement For A Grid-Scale Offshore Hybrid Wind-Solar Project In Italy.

- I can understand Italy, but surely a solar farm in the Dutch waters of the North Sea, is being at least slightly optimistic.

But the home page of the Oranjewind web site, does have a mission statement of Blueprint For The New Generation Of Offshore Wind Farms.

Under a heading of The Perfect Match, this is said.

RWE’s OranjeWind offshore wind farm will be located 53 kilometers from the Dutch coast. To tackle the challenges of fluctuating power generation from wind and flexible energy demand, RWE has developed a blueprint for the integration of offshore wind farms in the Dutch energy system.

A combination of smart innovations and investments will be used to realise this perfect match between supply and demand.

Under Innovations At OranjeWind, this is said.

In order to realise system integration and accelerate the energy transition, RWE is working together with a number of innovators on new developments in offshore wind farms. The company is realising and testing these innovations in the OranjeWind wind farm.These innovations include offshore floating solar, a subsea lithium-ion battery, LiDAR power forecasting system and a subsea hydro storage power plant off-site.

These technologies have their own sections, which give more information.

- Subsea Pumped Hydro Storage Power Plant (Ocean Grazer)

- Floating Solar (SolarDuck)

- Intelligent Subsea Energy Storage (Verlume)

- LiDAR-based Power Forecasting (ForWind, University of Oldenburg)

The web site also says this about knowledge from OranjeWind.

There is a lot to learn in an innovative project such as OranjeWind. While developing the wind farm, RWE started the OranjeWind Knowledge programme. This programme aims to generate and share knowledge to accelerate the energy transition.

In strong partnerships with TNO and Dutch universities, research is carried out in parallel to the development and operation of OranjeWind. By sharing research results, lessons learned, and relevant in-house expertise, RWE aims to close knowledge gaps and provide valuable insights in key focus areas for system integration. The generated knowledge will become openly available to educational and research institutes, governments and the market.

To ensure the dissemination of knowledge, RWE will actively partner with educational institutions of all levels across the Netherlands. These partnerships allow RWE to share its expertise and provide the future workforce with the knowledge and skills needed to enable the energy transition.

It certainly appears that RWE intends to get as much out of this project as they can.

I don’t think that they can be criticised for that objective.

Iberdrola Preparing Two East Anglia Offshore Wind Projects For UK’s Sixth CfD Round

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

ScottishPower Renewables, Iberdrola’s company in the UK, is getting the East Anglia One North and East Anglia Two offshore wind projects ready for the upcoming auction round for Contracts for Difference (CfD).

These three paragraphs give more details.

This is according to project updates Iberdrola published as part of its financial results for 2023.

Iberdrola says “good progress is being made in the key engineering and design work” for the two projects and, while they were not presented in the UK’s fifth CfD Allocation Round (AR5), preparations are being made to take part in Allocation Round 6 (AR6).

The two offshore wind farms are part of the GBP 6.5 billion (around EUR 7.6 billion) East Anglia Hub project, which also includes East Anglia Three, currently in construction and expected to start delivering electricity in 2026. The 1.4 GW East Anglia Three was awarded Contract for Difference in July 2022.

It is now possible to build a table of Iberdrola’s East Anglian Hub.

- East Anglia One – 714 MW – Commissioned in 2020.

- East Anglia One North – 800 MW – To be commissioned in 2026.

- East Anglia Two – 900 MW – To be commissioned in 2026.

- East Anglia Three – 1372 MW – To be commissioned in 2026.

Note.

- East Anglia One is the largest windfarm in Iberdrola’s history

- These four wind farms are connected to the shore at Bawdsey on the River Deben.

These wind farms are a total of 3786 MW.

In addition there are RWE’s three Norfolk wind farms.

- Norfolk Boreas – 1386 MW – To be commissioned in 2027.

- Norfolk Vanguard East – 1380 MW – To be commissioned before 2030.

- Norfolk Vanguard West – 1380 MW – To be commissioned before 2030.

These wind farms are a total of 4146 MW, with a grand total of 7932 MW.

What Will Happen To The Electricity?

Consider.

- It is a lot of electricity.

- The good people of Norfolk are already protesting about the cables and pylons, that will connect the electricity to the National Grid.

- The good people of Suffolk will probably follow, their Northern neighbours.

- The wind farms are owned by Spanish company; Iberdrola and German company; RWE.

I wonder, if someone will build a giant electrolyser at a convenient place on the coast and export the hydrogen to Europe by pipeline or tanker.

- The ports of Felixstowe, Great Yarmouth and Lowestoft could probably handle a gas tanker.

- The Bacton gas terminal has gas pipelines to Belgium and The Netherlands.

In addition, there are various electricity interconnectors in use or under construction, that could send electricity to Europe.

- National Grid’s Lion Link to the Netherlands.

- NeuConnect to Germany from the Isle of Grain.

Whoever is the UK’s Prime Minister in 2030 will reap the benefits of these East Anglian and Norfolk wind farms.

In addition.

- The Hornsea wind farm will have tripled in size from 2604 MW to 8000 MW.

- The Dogger Bank wind farm will have grown from 1235 MW to 8000 MW.

- There is 4200 MW of wind farms in Morecambe Bay and around England.

They would be so lucky.

RWE And National Grid Answer New York Offshore Wind Call

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

Community Offshore Wind, a joint venture of RWE and National Grid Ventures, has submitted a proposal to the New York State Energy Research and Development Authority (NYSERDA) to develop 1.3 GW of new offshore wind capacity in response to New York’s expedited fourth competitive offshore wind solicitation.

These four paragraphs add more details.

This next phase of the project builds upon Community Offshore Wind’s provisional offtake award to deliver 1.3 GW of wind capacity as part of New York’s third solicitation for offshore wind. In total, the projects are expected to generate USD 4.4 billion in economic benefits to New York.

Combined with its provisionally awarded New York project, Community Offshore Wind is on track to deliver nearly USD 100 million in workforce and economic development investments, the developer said.

The new proposal includes nearly USD 50 million in funding for workforce and community initiatives, with a focus on creating opportunities for diverse New Yorkers and supporting local non-profit organizations.

The proposal also includes an investment of up to USD 10 million in the offshore wind supply chain, to help New York businesses prepare for the economic opportunities the growing industry will create. All of these commitments are contingent on NYSERDA’s final selections.

is this partly a result of the meeting between Energy Security Secretary Claire Coutinho and Germany’s Vice Chancellor, Robert Habeck, that I wrote abut in UK And Germany Boost Offshore Renewables Ties?

We certainly seem to be getting some good deals on renewable energy these days with the Germans and the Koreans.

Perhaps someone in the government is doing something right?

Enabling The UK To Become The Saudi Arabia Of Wind?

The title of this post, is the same as that of a paper from Imperial College.

The paper can be downloaded from this page of the Imperial College web site.

This is a paragraph from the Introduction of the paper.

In December 2020, the then Prime Minister outlined the government’s ten-point plan for a green industrial revolution, expressing an ambition “to turn the UK into the Saudi Arabia of wind power generation, enough wind power by 2030 to supply every single one of our homes with electricity”.

The reference to Saudi Arabia, one of the world’s largest oil producers for many decades, hints at the significant role the UK’s energy ambitions hoped to play in the global economy.

Boris Johnson was the UK Prime Minister at the time, so was his statement just his usual bluster or a simple deduction from the facts.

The paper I have indicated is a must-read and I do wonder if one of Boris’s advisors had read the paper before Boris’s speech. But as the paper appears to have been published in September 2023, that is not a valid scenario.

The paper though is full of important information.

The Intermittency Of Wind And Solar Power

The paper says this about the intermittency of wind and solar power.

One of the main issues is the intermittency of solar and wind electricity generation, which means it cannot be relied upon without some form of backup or sufficient storage.

Solar PV production varies strongly along both the day-night and seasonal cycles. While output is higher during the daytime (when demand is

higher than overnight), it is close to zero when it is needed most, during the times of peak electricity demand (winter evenings from 5-6 PM).At present, when wind output is low, the UK can fall back to fossil fuels to make up for the shortfall in electricity supply. Homes stay warm, and cars keep moving.

If all sectors were to run on variable renewables, either the country needs to curb energy usage during shortfalls (unlikely to be popular with consumers), accept continued use of fossil fuels across all sectors (incompatible with climate targets), or develop a large source of flexibility such as energy storage (likely to be prohibitively expensive at present).

The intermittency of wind and solar power means we have a difficult choice to make.

The Demand In Winter

The paper says this about the demand in winter.

There are issues around the high peaks in heating demand during winter, with all-electric heating very expensive to serve (as

the generators built to serve that load are only

needed for a few days a year).Converting all the UK’s vehicles to EVs would increase total electricity demand from 279 TWh to 395 TWh. Switching all homes across the country to heat pumps would increase demand by a further 30% to 506 TWh.

This implies that the full electrification of the heating and transport sectors would increase the annual power needs in the country by 81%.

This will require the expansion of the electricity system (transmission capacity, distribution grids, transformers,

substations, etc.), which would pose serious social, economic and technical challenges.Various paths, policies and technologies for the decarbonisation of heating, transport, and industrial emissions must be considered in order for the UK to meet its zero-emission targets.

It appears that electrification alone will not keep us warm, power our transport and keep our industry operating.

The Role Of Hydrogen

The paper says this about the role of hydrogen.

Electrifying all forms of transport might prove difficult (e.g., long-distance heavy goods) or nigh impossible (e.g., aviation) due to the high energy density requirements, which current batteries cannot meet.

Hydrogen has therefore been widely suggested as a low-carbon energy source for these sectors, benefiting from high energy density (by weight), ease of storage (relative to electricity) and its versatility to be used in many ways.

Hydrogen is also one of the few technologies capable of

providing very long-duration energy storage (e.g., moving energy between seasons), which is critical to supporting the decarbonisation of the whole energy system with high shares of renewables because it allows times of supply and demand mismatch to be managed over both short and long timescales.It is a clean alternative to fossil fuels as its use (e.g., combustion) does not emit any CO2.

Hydrogen appears to be ideal for difficult to decarbonise sectors and for storing energy for long durations.

The Problems With Hydrogen

The paper says this about the problems with hydrogen.

The growth of green hydrogen technology has been held back by the high cost, lack of existing infrastructure, and its lower efficiency

of conversion.Providing services with hydrogen requires two to three times more primary energy than direct use of electricity.

There is a lot of development to be done before hydrogen is as convenient and affordable as electricity and natural gas.

Offshore Wind

The paper says this about offshore wind.

Offshore wind is one of the fastest-growing forms of renewable energy, with the UK taking a strong lead on the global stage.

Deploying wind turbines offshore typically leads to a higher electricity output per turbine, as there are typically higher wind speeds and fewer obstacles to obstruct wind flow (such as trees and buildings).

The productivity of the UK’s offshore wind farms is nearly 50% higher than that of onshore wind farms.

Offshore wind generation also typically has higher social acceptability as it avoids land usage conflicts and has a lower visual impact.

To get the most out of this resource, very large structures (more than twice the height of Big Ben) must be connected to the ocean floor and operate in the harshest conditions for decades.

Offshore wind turbines are taller and have larger rotor diameters than onshore wind turbines, which produces a more consistent and higher output.

Offshore wind would appear to be more efficient and better value than onshore.

The Scale Of Offshore Wind

The paper says this about the scale of offshore wind.

The geographical distribution of offshore wind is heavily skewed towards Europe, which hosts over 80% of the total global offshore wind capacity.

This can be attributed to the good wind conditions and the shallow water depths of the North Sea.

The UK is ideally located to take advantage of offshore wind due to its extensive resource.

The UK could produce over 6000 TWh of electricity if the offshore wind resources in all the feasible area of the exclusive economic zone (EEZ) is exploited.

Note.

- 6000 TWh of electricity per annum would need 2740 GW of wind farms if the average capacity factor was a typical 25 %.

- At a price of 37.35 £/MWh, 6000 TWh would be worth $224.1 billion.

Typically, most domestic users seem to pay about 30 pence per KWh.

The Cost Of Offshore Wind

The paper says this about the cost of offshore wind.

The cost of UK offshore wind has fallen because of the reductions in capital expenditure (CapEx), operational expenditure (OpEx), and financing costs.

This has been supported by the global roll-out of bigger offshore wind turbines, hence, causing an increase in offshore wind energy capacity.

This increase in installed capacity has been fuelled by several low-carbon support schemes from the UK government.

The effect of these schemes can be seen in the UK 2017 Contracts for Difference (CfD) auctions where offshore wind reached strike prices as low as 57.50 £/MWh and an even lower strike price of 37.35 £/MWh in 2022.

Costs and prices appear to be going the right way.

The UK’s Offshore Wind Targets

The paper says this about the UK’s offshore wind targets.

The offshore wind capacity in the UK has grown over the past decade.

Currently, the UK has a total offshore wind capacity of 13.8GW, which is sufficient to power more than 10 million homes.

This represents a more than fourfold increase compared to the capacity installed in 2012.

The UK government has set ambitious targets for offshore wind development.

In 2019, the target was to install a total of 40 GW of offshore wind capacity by 2030, and this was later raised to 50 GW, with up to 5 GW of floating offshore wind.

This will play a pivotal role in decarbonising the UK’s power system by the government’s deadline of 2035.

As I write this, the UK’s total electricity production is 31.8 GW. So 50 GW of wind will go a good way to providing the UK with zero-carbon energy. But it will need a certain amount of reliable alternative power sources for when the wind isn’t blowing.

The UK’s Hydrogen Targets

The paper says this about the UK’s hydrogen targets.

The UK has a target of 10 GW of low-carbon hydrogen production to be deployed by 2030, as set out in the British Energy Security Strategy.

Within this target, there is an ambition for at least half of the 10 GW of production capacity to be met through green hydrogen production technologies (as opposed to hydrogen produced from steam methane reforming using carbon capture).

Modelling conducted by the Committee on Climate Change in its Sixth Carbon Budget estimated that demand for low-carbon hydrogen across the whole country could reach 161–376 TWh annually by 2050, comparable in scale to the total electricity demand.

We’re going to need a lot of electrolyser capacity.

Pairing Hydrogen And Offshore Wind

The paper says this about pairing hydrogen and offshore wind.

Green hydrogen holds strong potential in addressing the intermittent nature of renewable generation sources, particularly wind and solar energy, which naturally fluctuate due to weather conditions.

Offshore wind in particular is viewed as being a complementary technology to pair with green hydrogen production, due to three main factors: a) the high wind energy capacity factors offshore, b) the potential for large-scale deployment and c) hydrogen as a supporting technology for offshore wind energy integration.

It looks like a match made in the waters around the UK.

The Cost Of Green Hydrogen

The paper says this about the cost of green hydrogen.

The cost of green hydrogen is strongly influenced by the price of the electrolyser unit itself.

If the electrolyser is run more intensively over the course of the lifetime of the plant, a larger volume of hydrogen will be produced and so the cost of the electrolyser will be spread out more, decreasing the cost per unit of produced hydrogen.

If the variable renewable electricity source powering the electrolyser has a higher capacity factor, this will contribute towards a

lower cost of hydrogen produced.Offshore wind in the UK typically has a higher capacity factor than onshore wind energy (up to 20%), and is around five times higher than solar, so pairing

offshore wind with green hydrogen production is of interest.

It would appear that any improvements in wind turbine and electrolyser efficiency would be welcomed.

The Size Of Wind Farms

The paper says this about the size of wind farms.

Offshore wind farms can also be larger scale, due to increased availability of space and reduced restrictions on tip heights due to planning permissions.

The average offshore wind turbine in the UK had a capacity of 3.6 MW in 2022, compared to just 2.5-3 MW for onshore turbines.

As there are fewer competing uses for space, offshore wind can not only have larger turbines but the wind farms can comprise many more turbines.

Due to the specialist infrastructure requirements for hydrogen transport and storage, and the need for economies of scale to reduce the costs of

production, pairing large-scale offshore wind electricity generation with green hydrogen

production could hold significant benefits.

I am not surprised that economies of scale give benefits.

The Versatility Of Hydrogen

The paper says this about the versatility of hydrogen.

Hydrogen is a highly adaptable energy carrier with numerous potential applications and has been anticipated by some as playing a key role in the future energy system, especially when produced through electrolysis.

It could support the full decarbonisation of “hard to decarbonise” processes within the UK industrial sector, offering a solution for areas which may be difficult to electrify or are heavily reliant on fossil fuels for high-temperature heat.

When produced through electrolysis, it could be paired effectively as an energy storage technology with offshore wind, with the potential to store energy across seasons with little to no energy degradation and transport low-carbon energy internationally.

The UK – with its significant offshore wind energy resources and targets – could play a potentially leading role in producing green hydrogen to both help its pathway to net zero, and potentially create a valuable export industry.

In RWE Acquires 4.2-Gigawatt UK Offshore Wind Development Portfolio From Vattenfall, I postulated that RWE may have purchased Vattenfall’s 4.2 GW Norfolk Zone of windfarms to create a giant hydrogen production facility on the Norfolk coast. I said this.

Consider.

- Vattenfall’s Norfolk Zone is a 4.2 GW group of wind farms, which have all the requisite permissions and are shovel ready.

- Bacton Gas terminal has gas pipelines to Europe.

- Sizewell’s nuclear power stations will add security of supply.

- Extra wind farms could be added to the Norfolk Zone.

- Europe and especially Germany has a massive need for zero-carbon energy.

The only extra infrastructure needing to be built is the giant electrolyser.

I wouldn’t be surprised if RWE built a large electrolyser to supply Europe with hydrogen.

The big irony of this plan is that the BBL Pipeline between Bacton and the Netherlands was built, so that the UK could import Russian gas.

Could it in future be used to send the UK’s green hydrogen to Europe, so that some of that Russian gas can be replaced with a zero-carbon fuel?

Mathematical Modelling

There is a lot of graphs, maps and reasoning, which is used to detail how the authors obtained their conclusions.

Conclusion

This is the last paragraph of the paper.

Creating a hydrogen production industry is a transition story for UK’s oil and gas sector.

The UK is one of the few countries that could produce more hydrogen than it consumes in hydrocarbons today.

It is located in the centre of a vast resource, which premediates positioning itself at the centre of the European hydrogen supply chains.

Investing now to reduce costs and benefit from the generated value of exported hydrogen would make a reality out of the ambition to become the “Saudi Arabia of Wind”.

Boris may or may not have realised that what he said was possible.

But certainly make sure you read the paper from Imperial College.

RWE Acquires 4.2-Gigawatt UK Offshore Wind Development Portfolio From Vattenfall

The title of this post, is the same as that of this press release from RWE.

These three bullet points, act as sub-headings.

- Highly attractive portfolio of three projects at a late stage of development, with grid connections and permits secured, as well as advanced procurement of key components

- Delivery of the three Norfolk Offshore Wind Zone projects off the UK’s East Anglia coast will be part of RWE’s Growing Green investment and growth plans

- Agreed purchase price corresponds to an enterprise value of £963 million

These two paragraphs outline the deal.

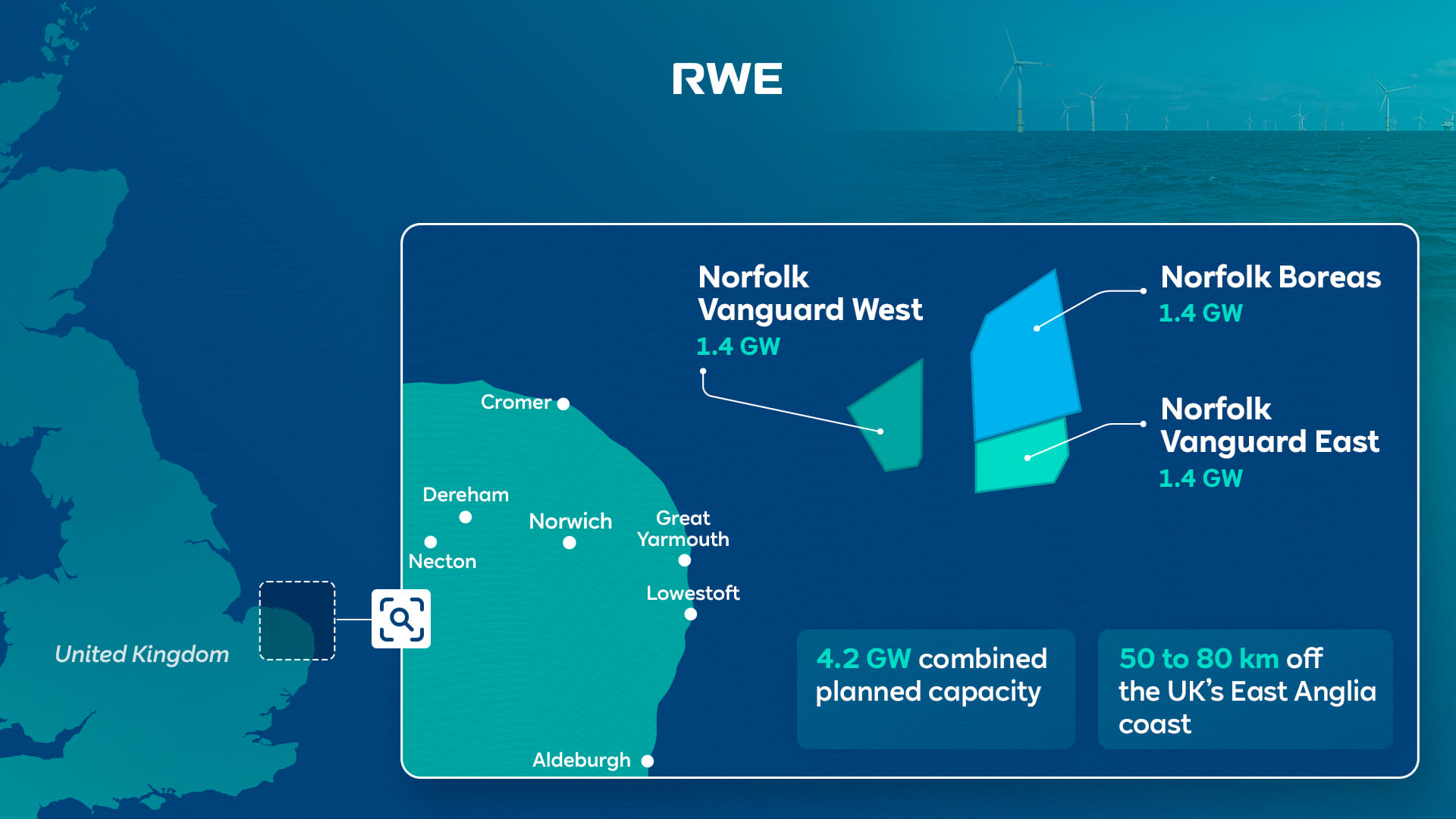

RWE, one of the world’s leading offshore wind companies, will acquire the UK Norfolk Offshore Wind Zone portfolio from Vattenfall. The portfolio comprises three offshore wind development projects off the east coast of England – Norfolk Vanguard West, Norfolk Vanguard East and Norfolk Boreas.

The three projects, each with a planned capacity of 1.4 gigawatts (GW), are located 50 to 80 kilometres off the coast of Norfolk in East Anglia. This area is one of the world’s largest and most attractive areas for offshore wind. After 13 years of development, the three development projects have already secured seabed rights, grid connections, Development Consent Orders and all other key permits. The Norfolk Vanguard West and Norfolk Vanguard East projects are most advanced, having secured the procurement of most key components. The next milestone in the development of these two projects is to secure a Contract for Difference (CfD) in one of the upcoming auction rounds. RWE will resume the development of the Norfolk Boreas project, which was previously halted. All three Norfolk projects are expected to be commissioned in this decade.

There is also this handy map, which shows the location of the wind farms.

Note that there are a series of assets along the East Anglian coast, that will be useful to RWE’s Norfolk Zone development.

- In Vattenfall Selects Norfolk Offshore Wind Zone O&M Base, I talked about how the Port of Great Yarmouth will be the operational base for the Norfolk Zone wind farms.

- Bacton gas terminal has gas interconnectors to Belgium and the Netherlands lies between Cromer and Great Yarmouth.

- The cable to the Norfolk Zone wind farms is planned to make landfall between Bacton and Great Yarmouth.

- Sizewell is South of Lowestoft and has the 1.25 GW Sizewell B nuclear power station, with the 3.2 GW Sizewell C on its way, for more than adequate backup.

- Dotted around the Norfolk and Suffolk coast are 3.3 GW of earlier generations of wind farms, of which 1.2 GW have connections to RWE.

- The LionLink multipurpose 1.8 GW interconnector will make landfall to the North of Southwold

- There is also the East Anglian Array, which currently looks to be about 3.6 GW, that connects to the shore at Bawdsey to the South of Aldeburgh.

- For recreation, there’s Southwold.

- I can also see more wind farms squeezed in along the coast. For example, according to Wikipedia, the East Anglian Array could be increased in size to 7.2 GW.

It appears that a 15.5 GW hybrid wind/nuclear power station is being created on the North-Eastern coast of East Anglia.

The big problem is that East Anglia doesn’t really have any large use for electricity.

But the other large asset in the area is the sea.

- Undersea interconnectors can be built to other locations, like London or Europe, where there is a much greater need for electricity.

- In addition, the UK Government has backed a consortium, who have the idea of storing energy by using pressurised sea-water in 3D-printed concrete hemispheres under the sea. I wrote about this development in UK Cleantech Consortium Awarded Funding For Energy Storage Technology Integrated With Floating Wind.

A proportion of Russian gas in Europe, will have been replaced by Norfolk wind power and hydrogen, which will be given a high level of reliability from Suffolk nuclear power.

I have some other thoughts.

Would Hydrogen Be Easier To Distribute From Norfolk?

A GW-range electrolyser would be feasible but expensive and it would be a substantial piece of infrastructure.

I also feel, that placed next to Bacton or even offshore, there would not be too many objections from the Norfolk Nimbys.

Hydrogen could be distributed from the site in one of these ways.

- By road transport, as ICI did, when I worked in their hydrogen plant at Runcorn.

- I suspect, a rail link could be arranged, if there was a will.

- By tanker from the Port of Great Yarmouth.

- By existing gas interconnectors to Belgium and the Netherlands.

As a last resort it could be blended into the natural gas pipeline at Bacton.

In Major Boost For Hydrogen As UK Unlocks New Investment And Jobs, I talked about using the gas grid as an offtaker of last resort. Any spare hydrogen would be fed into the gas network, provided safety criteria weren’t breached.

I remember a tale from ICI, who from their refinery got a substantial amount of petrol, which was sold to independent petrol retailers around the North of England.

But sometimes they had a problem, in that the refinery produced a lot more 5-star petrol than 2-star. So sometimes if you bought 2-star, you were getting 5-star.

On occasions, it was rumoured that other legal hydrocarbons were disposed of in the petrol. I was once told that it was discussed that used diluent oil from polypropylene plants could be disposed of in this way. But in the end it wasn’t!

If hydrogen were to be used to distribute all or some of the energy, there would be less need for pylons to march across Norfolk.

Could A Rail Connection Be Built To The Bacton Gas Terminal

This Google Map shows the area between North Walsham and the coast.

Note.

- North Walsham is in the South-Western corner of the map.

- North Walsham station on the Bittern Line is indicated by the red icon.

- The Bacton gas terminal is the trapezoidal-shaped area on the coast, at the top of the map.

ThisOpenRailwayMap shows the current and former rail lines in the same area as the previous Google Map.

Note.

- North Walsham station is in the South-West corner of the map.

- The yellow track going through North Walsham station is the Bittern Line to Cromer and Sheringham.

- The Bacton gas terminal is on the coast in the North-East corner of the map.

I believe it would be possible to build a small rail terminal in the area with a short pipeline connection to Bacton, so that hydrogen could be distributed by train.

There used to be a branch line from North Walsham station to Cromer Beach station, that closed in 1953.

Until 1964 it was possible to get trains to Mundesley-on-Sea station.

So would it be possible to build a rail spur to the Bacton gas terminal along the old branch line?

In the Wikipedia entry for the Bittern Line this is said.

The line is also used by freight trains which are operated by GB Railfreight. Some trains carry gas condensate from a terminal at North Walsham to Harwich International Port.

The rail spur could have four main uses.

- Taking passengers to and from Mundesley-on-Sea and Bacton.

- Collecting gas condensate from the Bacton gas terminal.

- Collecting hydrogen from the Bacton gas terminal.

- Bringing in heavy equipment for the Bacton gas terminal.

It looks like another case of one of Dr. Beeching’s closures coming back to take a large chunk out of rail efficiency.

Claire Coutinho And Robert Habeck’s Tete-a-Tete

I wrote about their meeting in Downing Street in UK And Germany Boost Offshore Renewables Ties.

- Did Habeck run the RWE/Vattenfall deal past Coutinho to see it was acceptable to the UK Government?

- Did Coutinho lobby for SeAH to get the contract for the monopile foundations for the Norfolk Zone wind farms?

- Did Coutinho have a word for other British suppliers like iTMPower.

Note.

- I think we’d have heard and/or the deal wouldn’t have happened, if there had been any objections to it from the UK Government.

- In SeAH To Deliver Monopiles For Vattenfall’s 2.8 GW Norfolk Vanguard Offshore Wind Project, I detailed how SeAH have got the important first contract they needed.

So it appears so far so good.

Rackheath Station And Eco-Town

According to the Wikipedia entry for the Bittern Line, there are also plans for a new station at Rackheath to serve a new eco-town.

This is said.

A new station is proposed as part of the Rackheath eco-town. The building of the town may also mean a short freight spur being built to transport fuel to fire an on-site power station. The plans for the settlement received approval from the government in 2009.

The eco-town has a Wikipedia entry, which has a large map and a lot of useful information.

But the development does seem to have been ensnared in the planning process by the Norfolk Nimbys.

The Wikipedia entry for the Rackheath eco-town says this about the rail arrangements for the new development.

The current rail service does not allow room for an extra station to be added to the line, due to the length of single track along the line and the current signalling network. The current service at Salhouse is only hourly during peak hours and two-hourly during off-peak hours, as not all trains are able to stop due to these problems. Fitting additional trains to this very tight network would not be possible without disrupting the entire network, as the length of the service would increase, missing the connections to the mainline services. This would mean that a new 15-minute shuttle service between Norwich and Rackheath would have to be created; however, this would interrupt the main service and cause additional platforming problems. Finding extra trains to run this service and finding extra space on the platforms at Norwich railway station to house these extra trains poses additional problems, as during peak hours all platforms are currently used.

In addition, the plans to the site show that both the existing and the new rail station, which is being built 300m away from the existing station, will remain open.

. As the trains cannot stop at both stations, changing between the two services would be difficult and confusing, as this would involve changing stations.

I feel that this eco-town is unlikely to go ahead.

Did RWE Buy Vattenfall’s Norfolk Zone To Create Green Hydrogen For Europe?

Consider.

- Vattenfall’s Norfolk Zone is a 4.2 GW group of wind farms, which have all the requisite permissions and are shovel ready.

- Bacton Gas terminal has gas pipelines to Europe.

- Sizewell’s nuclear power stations will add security of supply.

- Extra wind farms could be added to the Norfolk Zone.

- Europe and especially Germany has a massive need for zero-carbon energy.

The only extra infrastructure needing to be built is the giant electrolyser.

I wouldn’t be surprised if RWE built a large electrolyser to supply Europe with hydrogen.

Major Boost For Hydrogen As UK Unlocks New Investment And Jobs

The title of this post, is the same as that of this press release from the Government.

These three bullet points, act as sub-headings.

-

Eleven new production projects will invest around £400 million up front over the next 3 years, growing the UK’s green economy

-

More than 700 jobs to be created, representing the largest number of commercial scale green hydrogen production projects announced at once anywhere in Europe

-

New certainty for industry as government sets out hydrogen ambitions, including future production, transport and storage rounds

These two paragraphs outline the investment.

Over 700 jobs will be created across the UK in a world-leading hydrogen industry from the South West of England to the Highlands of Scotland, backed by £2 billion in government funding over the next 15 years.

Energy Security Secretary Claire Coutinho today (Thursday 14 December) announced backing for 11 major projects to produce green hydrogen – through a process known as electrolysis – and confirmed suppliers will receive a guaranteed price from the government for the clean energy they supply.

Note.

- This represents the largest number of commercial scale green hydrogen production projects announced at once anywhere in Europe.

- It is green hydrogen produced by electrolysis.

- The projects appear to be distributed around the UK.

- 125 MW of new hydrogen for businesses will be delivered.

I detailed the shortlist in Hydrogen Business Model / Net Zero Hydrogen Fund: Shortlisted Projects Allocation Round 2022, which used this press release from the Government as source.

Projects And Topics

This notice from the Government lists the eleven successful projects.

Projects and topics mentioned in the notice include.

Bradford Low Carbon Hydrogen

I was very impressed, when I went to see the public exhibition of this project.

- One of the reasons for building the electrolyser, is that Bradford has too many steep hills for electric buses, so will have to use more powerful hydrogen buses.

- I also got talking to a Bradford councillor, who said that they were going to use hydrogen to attract businesses to the city.

- It’s also rather large with a capacity of 24.5 MW.

The press release also gives this comment from Gareth Mills, Managing Director at N-Gen who said.

This is an important and exciting project, not just for Bradford, but also for the wider area and the community that lives here, so we are delighted to now have financial backing from government to allow us to start work on the site.

Bradford Council declared a climate emergency in 2019 and we believe this facility will play an important role in helping the area deliver on its climate change ambitions.

We know hydrogen can support decarbonising all energy types including transport, and producing green hydrogen is central to this, so we’re really excited to work with Hygen to deliver this development.

I very much feel that other large towns and cities will follow Bradford’s example.

Carlton Power

Carlton Power is a developer, who have been successful with bids for three hydrogen production projects.

- Barrow Green Hydrogen – 21 MW

- Langage Green Hydrogen – 7 MW

- Trafford Green Hydrogen – 10.5 MW

The links go to the respective web sites.

The press release also gives this comment from Eric Adams, Carlton Power’s Hydrogen Projects Director who said.

We are delighted with today’s announcement from the Department for Energy Security and Net Zero (DESNZ). Securing contracts for each project – totalling 55MW of capacity and an investment of c£100 million, and each with planning consent – is a major achievement and places Carlton Power among the leading British companies that are helping to build the hydrogen economy in the UK.

The press release also gives this comment from Keith Clarke, Founder and Chief Executive of Carlton Power who said.

We are supporting UK industry to decarbonise their operations, supporting the UK’s efforts to reach net zero and we are a catalyst for green investment and jobs into the UK regions. Working with our financial partners, Schroders Greencoat, we can now work towards Final Investment Decisions for each scheme in the early part of next year and thereafter work to have the 3 enter commercial operation within 2 years.

Carlton Power seem pleased, they got all the projects, they wanted.

Cromarty Hydrogen Project

The Cromarty Hydrogen Project has a web site, where this is said about the background of the project.

This Proposed Development would form part of the North of Scotland Hydrogen Programme recognised in the Scottish Government’s Hydrogen Action Plan1 The North of Scotland Hydrogen Programme is a strategic programme in line with the Scottish Government’s resolve to achieve Net Zero greenhouse gas (GHG) emissions by 2045 and the UK Government’s ambition by 2050. The programme is aimed at developing hydrogen production hubs across the North of Scotland to supply hydrogen, initially to meet industrial and heavy goods vehicle (HGV) transport demand in the near term and then expand to cater to additional hydrogen demands in the future.

The Cromarty Hydrogen Project is the first project in the Scotland Hydrogen Programme. It originated from a collaboration between the Port of Cromarty Firth, ScottishPower, Glenmorangie, Whyte & Mackay and Diageo and the project originator, Storegga during the feasibility stage. This project is looking to develop a green hydrogen production hub in the Cromarty Firth region and revolves around the local distilleries forming the baseload demand for early phases of the project, which would enable them to decarbonise in line with their own ambitions and sector targets.

Note.

- In Cromarty Firth And Forth To Host First Green Freeports, I talk about how Cromarty Firth is going to be a green freeport.

- The electrolyser is a medium-sized one at 10.6 MW.

- Initially HGVs will take a large part of the output.

The distillers seem to be playing a large part. I assume it it’s because distilling needs a lot of heat to boil off all the water from a spirit.

The press release also gives this comment from Sarah Potts, Storegga’s Hydrogen Managing Director, who said.

After a lot of hard work by the integrated Storegga and ScottishPower project team, particularly over the past 18 months since the UK government launch of HAR1, I’m delighted that Cromarty has been selected by the UK government Department of Energy Security and Net Zero as one of 11 projects to be awarded a funding support contract. As an SME originating from North East Scotland, I believe Storegga is able to bring a unique perspective and ambition to deliver decarbonisation solutions for Scottish industry. We look forward to now being able to take the project forward to a final investment decision in 2024, with first production in 2026 and continuing to grow our hydrogen investments in the region.

The Cromarty Hydrogen Project appears to be a local project developed to satisfy a local need, but within Government policy.

Green Hydrogen 3

I wrote about this project in Government Hydrogen Boost To Help Power Kimberly-Clark Towards 100% Green Energy Target.

It is being developed by HYRO at Northfleet for Kimberly-Clark.

The press release also gives this comment from Alex Brierley, co-head of Octopus Energy Generation’s fund management team, who said.

This is a major milestone as this funding will enable HYRO to roll out green hydrogen projects at scale in hard-to-electrify industrial processes. Our first project will be working with Kimberly-Clark to flush away fossil fuels when manufacturing Andrex and Kleenex. We’ve got a big pipeline of projects to help even more industrial businesses decarbonise – and we’re on track to invest billions in this sector.

Note.

- Will Andrex become the bog-roll of choice for the supporters of Extinction Rebellion and Just Stop Oil?

- Octopus Energy seem to be getting their fingers into lots of projects.

- I suspect that Octopus Energy will need billions.

I very much like the way that Kimberly-Clark are going and it will be interesting, if they bring out a sales philosophy based on low-carbon manufacture.

Hydrogen Blending

The press release talks of hydrogen blending.

Ministers have also announced their decision to support hydrogen blending in certain scenarios – subject to an assessment of safety evidence and final agreement.

Currently, less than 1% of the gas in distribution networks is hydrogen. Under proposals, hydrogen could be blended with other gases in the network as an offtaker of last resort, working to reduce costs in the hydrogen sector by helping producers, and to support the wider energy system.

Hydrogen blending may help achieve the UK’s net zero ambitions, but would have a limited and temporary role as the UK moves away from the use of natural gas.

When I was a wet-behind-the-ears young engineer working on ICI’s hydrogen plant at Runcorn in the 1960s, one of the topics over coffee was how can ICI find more markets for the hydrogen they produce. I suspect a lot of the excess hydrogen went to raise steam in ICI’s power station. That wasn’t very efficient or profitable.

But suppose it is deemed safe to have up to 5 % of hydrogen in the natural gas supply. Then an electrolyser operator, would know they have an offtaker of last resort, which would in effect set a minimum price for the hydrogen.

- I believe this could help their sales of hydrogen to heavy gas users, within easy reach by pipeline or truck of the electrolyser.

- It might also attract businesses with a heavy energy usage or large carbon emissions to relocate close to an electrolyser.

Allowing hydrogen blending will also mean that no expensive hydrogen is wasted.

The government’s proposal on hydrogen blending is very sensible.

Hydrogen In Home Heating

The press release says this about using hydrogen for home heating.

Ministers have decided not to proceed with a hydrogen trial in Redcar, as the main source of hydrogen will not be available. The government recognises the potential role of hydrogen in home heating and will assess evidence from the neighbourhood trial in Fife, as well as similar schemes across Europe, to decide in 2026 whether and how hydrogen could help households in the journey to net zero.

I believe the ideal way to heat homes and other buildings depends on what is available at the building’s location.

Promising ideas are coming through, but I haven’t seen one that will suit my circumstances.

But something will come through and my engineering instinct says it will be powered by natural gas and the carbon will be captured. The system would probably work on a district-wide basis.

HyMarnham

HyMarnham is probably the most unusual of the projects.

It is a collaboration between J G Pears and GeoPura.

J G Pears describe themselves like this on their web site.

JG Pears is one of the UK’s leading processors of animal by-products and food waste. Pioneering environmentally-aware practices since we started out in 1972, we play a vital role in the agricultural and food industries.

GeoPura has this mission statement on their web site.

GeoPura has a totally zero-emissions answer to how we’re going to generate, store and distribute the vast amount of energy required to decarbonise our global economies. Clean fuels. Green fuels. We believe that renewable energy is the future.

It appears that a 9.3 MW electrolyser will be built on the site of the demolished High Marnham coal-fired power station, which is shown on this Google Map.

Note.

- The River Trent runs North-South across the map.

- There are two villages of High and Low Marnham in the middle of the map.

- The circles at the top of the map indicate the cooling towers of the demolished High Marnham power station.

- The High Marnham power station site is now owned by J G Pears.

- J G Pears Newark site is to the West of Low Marnham village.

- In the North-East corner of the map is the Fledborough viaduct, which crosses the River Trent.

- Network Rail’s High Marnham Test Track runs East-West across the map and uses the Fledborough viaduct to cross the Trent.

This second Google Map shows a close up of the former power station site.

Note.

- Network Rail’s High Marnham Test Track runs East-West across the map at the top.

- The remains of High Marnham power station can be clearly seen.

- The sub-stations that connected the power station to the grid are still in place.

This article on Energy-Pedia is entitled UK: HyMarnham Power’s Green Hydrogen Project Shortlisted for UK’s Net Zero Hydrogen Fund and contains this paragraph.

Harnessing the expertise of GeoPura and JG Pears, the site will be powered by 43 MW of new solar energy and utilises 8MW of electrolysers; establishing a long-term supply of low carbon hydrogen in the region.

Note that the electrolysers are now sized at 9.3 MW.

It looks to me like one or both companies wanted an electrolyser and J G Pears had the site, so engineers and executives of the two companies got together in a decent real ale pub, started thinking and the result is HyMarnham.

- Electricity can come from the solar panels or the National Grid.

- Excess solar electricity can be exported through the National Grid.

- There is plenty of space on the site for a hydrogen filling station for vehicles.

- There could even be a filling point for refueling hydrogen-powered trains on the High Marnham Test Track.

The Energy-Pedia article indicates that GeoPura and JG Pears would like to get started this year.

Could the partners install a small electrolyser linked to the National Grid, initially, so that Network Rail has the ability to test hydrogen trains?

InchDairnie Distillery In Scotland

I have just looked at the InchDairnie Distillery web site.

- It looks a high class product.

- The company is best described as Scotch Whisky Reimagined.

- The company is based in Fife near Glenrothes.

- They appear to have just launched a rye whisky, which they are aiming to export to Canada, Japan and Taiwan.

The press release says this about InchDairnie.

InchDairnie Distillery in Scotland, who plan to run a boiler on 100% hydrogen for use in their distilling process.

That would fit nicely with the image of the distillery.

I suspect the hydrogen will be brought in by truck.

But would a zero-carbon whisky be a hit at Extinction Rebellion and Just Stop Oil parties?

PD Ports In Teesside

The press release says this about PD Ports.

PD Ports in Teesside, who will use hydrogen to replace diesel in their vehicle fleet, decarbonising port operations from 2026

I’ve felt for some time, that ports and freight interchanges, where you have lots of cranes, trucks and other diesel-powered equipment running hither and thither, is a good application for hydrogen, as not only does it cut carbon-emissions, but it also provides cleaner air for the workforce.

PD Ports have a Wikipedia entry, where this is said about their operations.

As of 2013 PD Ports owns and operates the Ports of Tees and Hartlepool under the name Teesport. The company also operates the Hull Container Terminal at the Port of Hull, and provides stevedoring and warehousing services at the Port of Immingham; logistics and warehousing at the Port of Felixstowe, Scunthorpe, and Billingham; and operates a wharf on the Isle of Wight. The company also owns the short sea ports in Scunthorpe (Groveport), Howden (Howdendyke, River Ouse, Yorkshire), and Keadby (River Trent).

The company appears to be bigger, than just Teesport and this project could grow.

The hydrogen for this project in Teesport appears to come from Tees Green Hydrogen, which will be a 5.2 MW facility developed by EDF Renewables Hydrogen.

The press release also gives this comment from Sopna Sury, Chief Operating Officer Hydrogen RWE Generation, who said.

Today’s announcements on the first 2 hydrogen allocation rounds mark a significant milestone in the development of the UK hydrogen economy. They represent a shift from policy development to project delivery, giving industry more clarity on the route to final investment decisions. Alongside the wider policy publications, this demonstrates that the UK wants to be a leader in delivering the clean energy transition.

These early projects are vital not only in driving the production of electrolytic hydrogen but also in signalling the need to build-out the T&S infrastructure for its wider distribution.

As a company with ambitions to develop approximately 2 gigawatts of green hydrogen projects across all our markets, and to invest around 8 billion euros net in green technologies in the UK between 2024-2030, RWE looks forward to being part of building a thriving hydrogen ecosystem in the UK.

These are positive words from the German energy company; RWE.

Sofidel In South Wales

The press release says this about Sofidel.

Sofidel in South Wales, who will replace 50% of their current gas boiler consumption with hydrogen at their Port Talbot paper mill.

The Wikipedia entry for the Sofidel Group has this first paragraph.

Sofidel is an Italian multinational producer of tissue paper for sanitary and domestic use. The Sofidel Group was founded in 1966. It is one of the world leaders in the tissue paper market and the second largest producer in Europe behind Essity. The privately held company is owned by the Stefani and Lazzareschi families, has subsidiaries in 13 countries and more than 6,600 employees.

Note.

- From the Wikipedia entry, it looks like the company has a good record on sustainability and has set itself good objectives.

- Sofidel are nor far from Tata Steel, who could be another large hydrogen user.

- Port Talbot will be a support port for the wind farms in the Celtic Sea.

- This is a typical hydrogen application, which reduces emission of carbon dioxide.

- But like me, have the Italian owners of the company been impressed with some of the Italian food, I’ve eaten in South Wales?

- Are British sweeteners better than Italian ones?

- The hydrogen for this project appears to come from HyBont Bridgend, which will be a 5.2 MW facility developed by Marubeni Europower.

The press release also gives this comment from Mr Tomoki Nishino, President and CEO of Marubeni Europower Ltd, who said.

Marubeni team is very honoured to be selected as a recipient of Hydrogen Allocation Round 1. Recently in October 2023, Marubeni signed an MoU with the UK government whereby we have shown our plan to invest £10 billion (along with our partners) into UK green business. We truly hope that a combination of HAR1 funding and Marubeni’s investment help decarbonize UK through HyBont, especially in the South Wales region.

It all seems to be happening in Port Talbot.

Tees Green Hydrogen

Tees Green Hydrogen is a 5.2 MW project being developed by EDF Renewables on Teesside.

The project has a web site, which has this project description on the home page.

Tees Green Hydrogen, will be a pioneering project, using the green electricity from nearby Teesside Offshore Wind Farm along with a new solar farm, which EDF Renewables UK intends to construct near Redcar, to power its hydrogen electrolyser.

The press release also gives this comment from Tristan Zipfel, Director of Strategy and Analysis at EDF Renewables UK, who said.

Today’s announcement is a huge leap forward for green hydrogen innovation which has the capacity to guarantee the long-term sustainability of industry in the North East. We are delighted that the government has given this vote of confidence in both EDF Renewables UK, Hynamics and the capacity of the region to be a world-leader in green technology and innovation.

The press release also gives this comment from Pierre de Raphelis-Soissan, CEO at Hynamics UK, who said.

This is a very important step towards realising the potential of Tees Green Hydrogen and making a ground breaking contribution to decarbonisation in the Tees Valley. The project is uniquely placed to be scalable in order that future demand can be met as hydrogen-based technology becomes the industrial norm.

Note.

- The project will be powered by both wind and solar.

- Hynamics is a subsidiary of EDF.

- I suspect that this project will supply PD Ports with hydrogen.

This project looks like it could be just a starter for 5.2 MW.

West Wales Hydrogen

West Wales Hydrogen is a 14.2 MW project being developed by H2 Energy and Trafigura in West Wales.

The best source of information is this must-watch Youtube video.

- The company appears to be able to lease you a hydrogen truck on a pay per mile basis, at the same price as a diesel truck.

- Get the finance right for your customers and yourself and everybody will be happy.

I know it will work, as I used to own half a company that leased a lot of trucks in Ipswich.

- My experience, also says the model would work with taxis, Transit-sized vans, company cars and vehicles like Defenders.

- It would also work very well around Ipswich, like my company did.

The press release also gives this comment from Julien Rolland, CEO of H2 Energy Europe, who said.

We are very grateful for the support that the UK government has announced for our 20MW electrolytic hydrogen production facility, marking a significant milestone in our journey to develop South Wales’s first large-scale green hydrogen production plant. The facility will enable industry in South Wales to transition to using green hydrogen produced from renewable energy sources.

The green hydrogen produced at Milford Haven will be used to displace natural gas and other fossil fuels in industrial and chemical processes and contribute to the decarbonisation of the local industry. The interest that we’ve already received from local industry means we are already reviewing the opportunity to scale up the facility.

I can see this model being applied all over the UK.

Whitelee Green Hydrogen

Whitelee Green Hydrogen is a 7.1 MW project being developed by Scottish Power close to the Whitelee Wind Farm.

The Whitelee Wind Farm has a comprehensive Wikipedia entry, where this is said about the future of the wind farm.

In May 2009, the Scottish Government granted permission for an extension to the wind farm to produce up to a further 130 megawatts of power, which would increase the total generating capacity of Whitelee to 452 MW.

In 2010 a 75 turbine extension commenced, adding an additional 217 MW of capacity, enough to power the equivalent of over 124,000 homes. This brought the total generating capacity of the wind farm up to 539 MW. Additionally, the extension added a further 44 km of trails to the site. John Sisk and Son Limited and Roadbridge were jointly appointed as Principal Contractors for the site during construction with Alstom Limited erecting and commissioning the wind turbines.

In August 2012 Scottish Power announced that it was applying for a further small extension of five turbines on the west of the existing site, adding 12 MW of capacity. This was refused by the DPEA on 19 Oct 2016.

A £21 million (US$29.35 million) 50MW/50MWh grid battery is being added to improve resource utilization, with plans for a 40 MW solar farm and a 20 MW hydrogen electrolyzer.

The press release also gives this comment from Peter Jones, Director of ScottishPower Green Hydrogen Business, who said.

The first wave of production facilities like Whitelee and Cromarty will demonstrate that zero-emission hydrogen can be delivered at commercial scale and drive the development of a viable market for the green fuel.

It will also create highly skilled green jobs across the UK and quickly support a world leading supply chain.

It’s early days for this burgeoning market and government support is to be welcomed to help deliver a future green hydrogen economy.

With 539 MW of wind, 40 MW of solar and a 50MW/50MWh grid battery to drive a 7.1 MW electrolyser, this should prove to be a reliable source of green hydrogen.

My Thoughts

I have a few extra thoughts.

Coverage Is Rather Patchy

Some areas of the UK don’t seem to be well-served with green hydrogen from this funding.

- East Suffolk with all those trucks going to and from the Port of Felixstowe. There’s certainly no lack of renewable energy.

- Humberside with all its energy-hungry industries. There’s certainly no lack of renewable energy.

- Hampshire with all those trucks going to and from the ports of Portsmouth and Southampton. But there is a lack of renewable energy.

- Lincolnshire with all those trucks going to and from Immingham. There’s certainly no lack of renewable energy.

- London with all those local trucks delivering building materials to sites all over the capital. But then the current Mayor doesn’t have a hydrogen policy.

I would assume, that some of these areas will be funded for hydrogen in the second round.

RWE’s Welsh Offshore Wind Project Powers Ahead

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

Natural Resources Wales has awarded marine licences for RWE’s Awel y Môr offshore wind project off the North Wales Coast.

These two paragraphs outline the project.

The offshore wind farm, which could power more than half of Wales’ homes, has secured all of its necessary planning approvals with the award of its marine licences from Natural Resources Wales, RWE said.

The marine licences have been awarded on behalf of Welsh Government ministers following the granting of a Development Consent Order in September.

With all the wind action in the East, we tend to forget that the Liverpool Bay area has a lot of wind.

- Awel y Môr – 500 MW – Before 2030

- Barrow – 90 MW – 2006

- Burbo Bank – 90 MW – 2007

- Burbo Bank Extension – 258 MW – 2017

- Gwynt y Môr – 576 MW – 2015

- Mona – 1500 MW – 2029

- Morecambe – 480 MW – 2028

- Morgan – 1500 MW – 2029

- North Hoyle – 60 MW – 2003

- Ormonde – 150 MW – 2012

- Rhyl Flats – 90 MW – 2009

- Walney – 367 MW – 2010

- Walney Extension – 659 MW – 2018

- West Of Duddon Sands – 389 MW – 2014

Note.

- This is a total of 6709 MW to be delivered before 2030.

- All the wind farms have fixed foundations.

- RWE have an interest in three of the Welsh wind farms.

The Times today has this article which is entitled Energy Minnow Sees Pathway To Irish Sea Gasfield Via London IPO, where these are the first three paragraphs.

An energy minnow that is seeking to develop a gasfield in the Irish Sea is planning to list on Aim, the junior London stock exchange, in an attempt to buck the downturn in initial public offerings.

EnergyPathways has announced its intention to float, seeking to raise at least £2 million.

It owns the rights to Marram, a small gasfield discovered in 1993 about 20 miles offshore from Blackpool. It is seeking permission from the government for its plan to develop the field in the Irish Sea quickly by connecting it with existing infrastructure that serves the already-producing gasfields in Morecambe Bay. It aims to be producing gas as soon as 2025.

This gasfield should produce enough gas until the large Liverpool Bay wind farms come on stream at the end of the decade.

RWE Partners With Masdar For 3 GW Dogger Bank South Offshore Wind Projects

The title of this post, is the same as that of this article on offshoreWIND.biz.

This is the sub-heading.

RWE has signed an agreement with UAE’s Masdar as a partner for its 3 GW Dogger Bank South (DBS) offshore wind projects in the UK.

These three paragraphs outline the deal.

The partners acknowledged the signing of the new partnership during a ceremony at COP28 in Dubai.

Masdar will acquire a 49 per cent stake in the landmark renewables projects while RWE, with a 51 per cent share, will remain in charge of development, construction, and operation throughout the life cycle of the projects.

RWE’s proposed DBS offshore wind project is made up of two offshore wind farms, Dogger Bank South East and Dogger Bank South West (DBS East and DBS West), each 1.5 GW, which are located over 100 kilometres offshore in the shallow area of the North Sea known as Dogger Bank.

Note.

- Masdar is an energy company headquartered in Abu Dubai.

- The Chairman of Masdar is President of COP28.

Does this deal indicate that wind farms are good investments for those individuals, companies and organisations with money?